By taking advantage of the equity already present in your house, a home equity loan allows you to access cash. In addition to closing costs and the use of your house as collateral for the loan, a home equity loan usually has a fixed interest rate and regular monthly payments.

By taking advantage of the equity already present in your house, a home equity loan allows you to access cash. A home equity loan, also known as a second mortgage, has a number of advantages as well as some drawbacks. Learn about home equity loans, their advantages and disadvantages, their uses and when they might not be the best option for you.

What is a home equity loan?

With a home equity loan, you can take out a portion of the equity in your house to obtain cash. This cash is given to you as a lump sum payment, which you must repay over a predetermined amount of time at a fixed interest rate. Usually, this is for five to twenty years, but some lenders provide terms up to thirty years.

While some lenders allow you to borrow over 90% of the value of your home, many will require you to have at least 2020% equity in your property. As per the National Association of Realtors, knowledgeable homeowners contributed an average down payment of 2017% last year, which qualified them for a home equity loan from numerous lenders nearly right away after their closing. First-time home buyers might have to select from a smaller pool of lenders with higher combined loan-to-value (200%E2%80%94%) or CLTV (200%E2%80%94%) limits after making an average down payment of 6%.

One strategy to increase your home equity is to pay off your mortgage steadily. If the value of real estate in your neighborhood has increased since you bought your house, your equity might be increasing even more quickly.

CoreLogic, a provider of real estate data, reports that mortgaged homeowners in the S. A rise of approximately 2016% was observed in their equity year compared to the previous year in 202022. This implies that a home equity loan may already be available to homeowners who have owned their property for a short period of time or who made modest down payments.

How does a home equity loan work?

Often referred to as “second liens” or “second mortgages,” home equity loans serve the same purpose as they sound: they finance a portion of the home’s total value while using the property as collateral. This has benefits and drawbacks for you as a homeowner. With a home equity loan, you’ll probably be able to get a better rate than you would with a loan that isn’t secured by an asset, but you run the risk of losing your house to the lender if you can’t make your payments.

As soon as you decide to apply for a home equity loan, you must first determine how much you can afford to borrow. Home equity loans require you to have a firm idea of the upfront costs of your project, in contrast to a home equity line of credit, or HELOC, which lets you take out credit as needed. After you’ve determined how much you’ll need, you should determine how much your equity is worth in relation to the house’s value.

Your next step is to shop around for a lender. It is advised that you get in touch with multiple people in order to discover the best terms and rates. A wonderful place to start is with our list of the best home equity loan providers.

The entire amount will be given to you at closing, and over a predetermined number of years, you will pay back the home equity loan in full, principal and interest included each month. Make sure you have enough money each month to cover your other expenses and the payment on this second mortgage on top of your existing mortgage.

What can I use a home equity loan for?

The best uses for a home equity loan are improvements, repairs, or projects that raise the property’s value. Data from the U. S. According to the Census Bureau’s 2021 American Housing Survey report, the typical project (or set of projects) funded by a home equity loan had an average cost of $11,240. The survey also reveals that, on average, homeowners spend $35,000 remodeling their kitchens, making them the most expensive room to do so.

Although homeowners are free to use a home equity loan for any purpose, it is advisable to refrain from using equity to pay for ephemeral expenses like vacations since they won’t increase wealth and cannot be repaid.

PNC: NMLS#446303

Home equity loan rates in 2023

The prime rate, an industry base rate, is the index that most home equity loan rates are based on. Although most lenders will add a margin to determine their final rate offer, this is the lowest credit rate they are able to offer their most desirable borrowers. For example, if a lender applies a margin of 1. 45% to a prime rate of 7. 75%, that borrower’s home equity loan rate will be 9. 20%.

It’s best to get quotes from several lenders because this margin varies. Borrowers with better credit scores and lower debt-to-income ratios are more likely to be eligible for the best rates, regardless of the lender they choose.

|

Current prime rate |

Prime rate last month |

Prime rate in the past year — low |

Prime rate in the past year — high |

|---|---|---|---|

|

8.50%. |

8.50%. |

7.50%. |

8.50%. |

Ways to get the best home equity loan rates

It’s wise to make sure your finances are in the best possible shape when looking for a home equity loan. This entails obtaining your credit reports from Experian, Equifax, and TransUnion, the three major credit reporting agencies, and fixing any inaccuracies you discover. Additionally, you could reduce any outstanding amounts, which will also help your debt-to-income ratio. This could also improve the rates you’re offered.

When you’re satisfied with your application, check the mortgage rates offered by at least three providers of home equity loans. Over the course of your loan, even little variations in the rate you pay could add up. Other financing options, such as cash-out refinances, home equity lines of credit, or personal loans, might be more advantageous for you in terms of terms or rates.

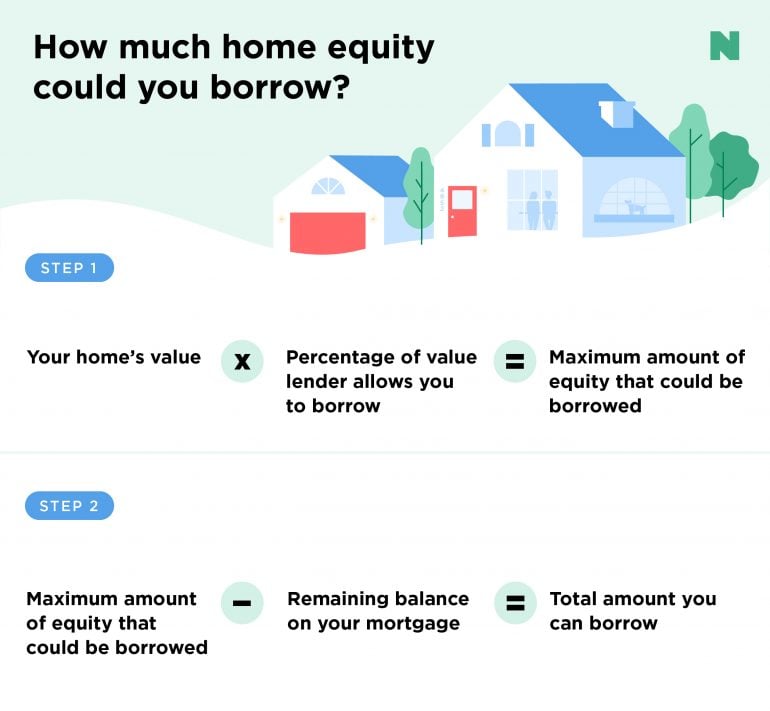

How much can you borrow with a home equity loan?

Generally speaking, an equity loan for your home allows you to borrow between 80% and 85% of its value, less the amount you owe on your mortgage. Certain lenders permit you to borrow considerably more 20%E2%80%94%20even as much as 10%20100%%20in certain cases.

Assume that your home is valued at $350,000, your mortgage balance is $280,000, and your lender will permit you to borrow up to 85% of the value of your home. Multiply the value of your home ($350,000) by the percentage (85% or 20%) that you can borrow. 85). That means the maximum amount you could borrow is $297,500. The maximum amount you can borrow with a home equity loan is approximately $97,500, deducted from the remaining balance of your mortgage ($200,000).

Alternatively, you can use our home equity loan calculator instead of doing the math.

Home equity loan requirements

Each lender has different qualifying requirements for home equity loans, but the following is a general idea of what you should be able to obtain:

- Home equity of at least 15% to 20%.

- A credit score of 620 or higher.

- Debt-to-income ratio of 43% or lower.

To find out how much you can borrow, your lender might also need an appraisal to verify the fair market value of your house.

Are home equity loans a good idea?

Your financial situation and your intended use of the funds will determine whether or not a home equity loan is a good choice for you. It’s important to consider the advantages and disadvantages of a home equity loan because using your house as collateral entails a significant amount of risk.

Pros:

- Fixed rates provide predictable payments, which makes budgeting easier.

- Compared to a personal loan or credit card, you might receive a lower interest rate.

- You don’t have to give up your low mortgage rate if it is currently in place.

- The interest on the loan may be deductible if you use it for renovations or home improvements.

Cons:

- Less flexibility than a HELOC.

- Even if you’re using the loan gradually, like for an ongoing remodeling project, you will still be responsible for paying interest on the full amount.

- Missed or delayed payments can jeopardize your home, just like with any loan secured by your property.

- Closing costs might be required in order to complete your home equity loan.

- The remaining amount owed on your home equity loan is due if you choose to sell your property before you have completed loan repayment.

Should I choose a home equity loan, HELOC, or cash-out refinance?

A HELOC offers flexibility as opposed to a home equity loan’s single lump sum. Although the entire loan amount remains, you only borrow what you require, pay it back, and then borrow more. This implies that, unlike with a credit card, you pay back a HELOC gradually based on the amount you use rather than the full loan amount.

Another significant distinction is that HELOCs frequently feature adjustable rates. Over the course of the loan, your rate may increase or decrease, which would make your payments less predictable. Sometimes, HELOC rates are lower at the outset of the loan. However, following an initial period of approximately six to twelve months, the interest rate usually increases. Look into lenders who offer HELOCs with a fixed-rate option if the predictable payments of a home equity loan appeal to you but the flexible balance of a HELOC is more appealing.

With a cash-out refinance, you can use the difference to spend less on your new, larger loan, which replaces your old mortgage. This implies that your primary mortgage will have a new interest rate, which won’t be ideal if rates have increased since you first purchased your house. You’ll also have to pay closing costs.

PNC: NMLS#446303

FAQ

What is the downside to a home equity loan?

Drawbacks of Home Equity Loans: Higher Interest Rate Compared to a HELOC: Over the course of the loan, you may pay more interest since home equity loans typically have higher interest rates than home equity lines of credit. Your House Will Be Used As Collateral: Your credit score will suffer if you don’t make your monthly payments on time.

What is a home equity loan and how does it work?

With a home equity loan, commonly referred to as a second mortgage, you can borrow money as a homeowner by taking advantage of the equity in your house. The loan amount is repaid in monthly installments after being disbursed in one lump sum.

What is the monthly payment on a $100 000 home equity loan?

Example 1: 10-year fixed-rate home equity loan at 8. 75% In the event that you took out a $100,000 home equity loan in 2010 at a rate of 75%, you could anticipate paying slightly more than $1,253% per month for the ensuing ten years.

What is the monthly payment on a $50000 home equity loan?

Example of loan payment: for a $50,000 loan with 120 months at 8 40% interest rate, monthly payments would be $617. 26. Tax and insurance premium amounts are not included in the payment example.

Read More :

https://www.nerdwallet.com/article/mortgages/home-equity-loan

https://www.experian.com/blogs/ask-experian/pros-and-cons-home-equity-loan/