One sort of loan that is secured by collateral, usually property, is called non-recourse debt. Even if the collateral does not fully cover the defaulted amount, the issuer may seize the collateral in the event of a borrower default and may not pursue additional compensation from the borrower. The borrower is not personally liable for a non-recourse debt.

Recourse vs. Non-Recourse Loans: An Overview

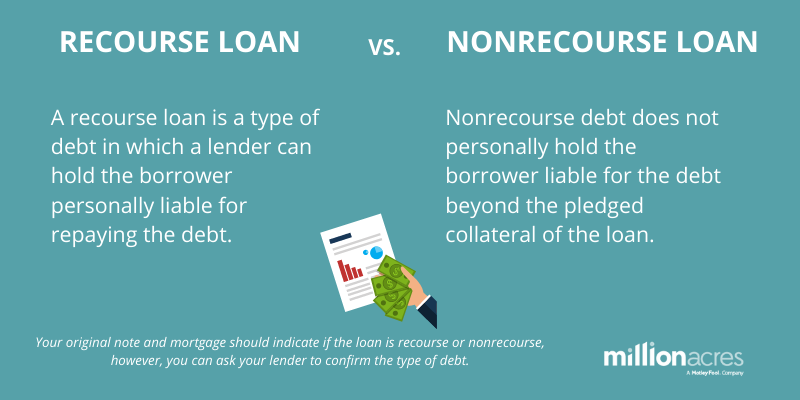

In the event that a borrower defaults on a loan and the debt balance exceeds the value of the collateral, a recourse loan enables a lender to pursue additional assets. With a non-recourse loan, the lender may only take possession of the collateral listed in the loan agreement, even if its worth is insufficient to pay off the whole debt.

Either type of loan may be collateralized. That is to say, the loan agreement will state that in the event of a default, the lender may seize and sell a specific property or properties belonging to the borrower in order to recover losses. But if the lender needs to recover its loan losses, a recourse debt gives it the right to pursue additional assets of the borrower in addition to the collateral’s value.

- There are two types of loans: recourse and non-recourse.

- Lenders may take possession of collateralized assets through recourse or non-recourse loans in the event that a borrower defaults on the loan.

- In the event that a borrower has not recovered all of their money after collateral is gathered, lenders offering recourse loans may pursue additional assets.

- In a non-recourse loan, lenders are able to seize collateral, but they are not legally permitted to seize the borrower’s other assets.

- Recourse loans won’t have the same terms, rates, or other restrictions as non-recourse loans.

Recourse Loans

Recourse loans have a lower interest rate than non-recourse loans. The lender will first seize and sell the collateral mentioned in the loan if the borrower defaults on the payment schedule and doesn’t fulfill their end of the bargain. The lender may pursue the borrower’s other assets or file a lawsuit to have the borrower’s wages garnished if that is not valuable enough to cover the loan balance.

Recourse loans mitigate the lender’s exposure to risk associated with less creditworthy borrowers. Lenders are able to charge a lower interest rate because they can lower the risk attached to these loans. This makes them more attractive to borrowers.

When foreclosure is finished, you will have to declare a capital gain or loss if you reject collateral that was offered for a recourse loan.

When banks and other financial institutions tighten their lending policies, these loans become more prevalent. For instance, the credit markets become more cautious and lenders raise their standards during difficult economic times.

Examples of Recourse Loans

Most automobile loans are recourse loans. The lender may seize the vehicle and sell it at fair market value if the borrower defaults. Cars lose a lot of value in the first few years of ownership, so this could be less than what is owed on the loan. If the borrower has any remaining debt, the lender may seize other assets to satisfy the balance owed.

Except for 12 states that permit both recourse and non-recourse mortgage loans, the majority of mortgage loans are recourse loans. These states are: Washington, Oregon, Texas, Utah, North Carolina, North Dakota, Alaska, Arizona, California, Connecticut, Idaho, and Minnesota.

It is significant to remember that in cases of default, especially by individuals, lenders do not always pursue assets beyond the collateral. Because asset seizure is costly and time-consuming, a lender may choose to write off a loss rather than pursue it further.

:max_bytes(150000):strip_icc()/dotdash-nonrecourse-loan-vs-recourse-loan-Final-2118fe68f30c4cfaaaeaacbded201963.jpg)

Non-Recourse Loans

Many banks do not offer non-recourse loans. It exposes them to losses in the event that their clients fall behind on their loans and their collateral is found to be insufficient. Lenders bear the loss if, upon selling the collateralized asset, there remains an outstanding balance. It is not entitled to any of the borrowers’ other assets, income, or possessions.

Although waiting for non-recourse loans may seem appealing to prospective borrowers, these loans typically have higher interest rates. Additionally, they are typically only granted to people and companies with excellent credit histories. Non-recourse loans are not free cards that can be repaid at any time; defaulting on one has consequences that can include losing the collateral, having one’s credit score negatively impacted, and possibly facing taxes.

The Internal Revenue Service views the relinquishment of collateral used for a non-recourse loan as a sale or exchange, and the amount is taxed as a capital gain or loss.

Example of a Non-Recourse Loan

As noted, many traditional banks avoid making non-recourse loans altogether. But a person or company with a stellar credit history could convince a lender to approve a non-recourse loan. It will come with a higher interest rate. Additionally, it might have stricter conditions, like a bigger down payment on a house or vehicle.

Do Banks Make Non-Recourse Loans?

Most banks do not offer non-recourse loans. Preferred borrowers may be eligible for them, but the terms and rates may be significantly higher than those of recourse loans.

What Is a Non-Recourse Loan and Who Benefits From It?

A loan that is non-recourse means that the lender can only pursue the collateral that was provided for the loan. Because the lender cannot seize additional assets to make up for lost revenue, this kind of loan is advantageous to the borrower.

What Is an Example of a Non-Recourse Loan?

Non-recourse mortgage laws are present in some states, like Texas and North Carolina. The lenders under these mortgage loans may foreclose on the home, but they are not permitted to try to take other assets to offset the loss.

Do You Have to Pay Back a Recourse Loan?

Recourse loans fall under the category of loans, and as such, they have terms and conditions that must be followed. The lender may seize additional assets to make up for lost money if the loan cannot be repaid in full with the interest stipulated in the agreement.

The Bottom Line

Since granting non-recourse loans exposes lenders to additional risk, most do not do so. On the other hand, banks might provide them to particular clients depending on their needs or financial situation. Consequently, non-recourse loans are probably going to have additional terms, like higher interest rates or larger down payments.

If you choose a recourse loan, you might be risking more than just your collateral in the event of default. When selecting a loan, think about your ability to repay the borrowed funds. Article Sources: Investopedia mandates that authors cite original sources to bolster their claims. These consist of government data, original reporting, white papers, and conversations with professionals in the field. When appropriate, we also cite original research from other respectable publishers. You can read more about the guidelines we adhere to when creating impartial, truthful content in our

FAQ

How does a non-recourse loan work?

With a nonrecourse debt (loan), the lender’s only option is to pursue the collateral. For instance, the bank can only foreclose on a home if a borrower defaults on a nonrecourse home loan. Generally speaking, the bank is unable to pursue additional legal action to recover the outstanding balance.

What are the disadvantages of a non-recourse loan?

Because non-recourse loans are riskier for lenders, they come with higher interest rates and are harder to qualify for. Although recourse loans carry greater risk for purchasers, their interest rates are lower.

Do you have to pay taxes on a non-recourse loan?

However, you won’t be required to pay taxes on the remaining debt in a nonrecourse scenario where your lender cancels it. Another tax-related issue to be aware of is that, should your lender sell your house for more than you still owe, you may still be required to pay taxes on any profits from the transaction.

Does non-recourse mean unsecured?

One sort of loan that is secured by collateral, usually property, is called non-recourse debt. Even if the collateral does not fully cover the defaulted amount, the issuer may seize the collateral in the event of a borrower default and may not pursue additional compensation from the borrower.

Read More :

https://www.investopedia.com/ask/answers/08/nonrecourse-loan-vs-recourse-loan.asp

https://www.investopedia.com/terms/n/nonrecoursedebt.asp