NerdWallet is an advertising partner for some or all of the mortgage lenders on our site; however, this has no bearing on our ratings, lender star ratings, or the order in which lenders appear on the page. Our opinions are our own. Here is a list of our partners.

A cash-out refinance allows you to obtain a new home loan that exceeds your existing balance. You receive the cash at closing for the difference between the amount of your new mortgage and the remaining balance on your old mortgage, which you can use for debt consolidation, home upgrades, or other expenses.

It’s crucial to consider the advantages and disadvantages before committing to a cash-out refinance, though, as you will now be repaying a larger loan with different terms, including a new mortgage rate.

How We Make Money

The businesses whose offers you see on this website pay us. Unless our mortgage, home equity, and other home lending products are specifically prohibited by law, this compensation may have an impact on how and where products appear on this website, including, for example, the order in which they may appear within the listing categories. However, this payment has no bearing on the content we post or the user reviews you see here. We don’t include the range of businesses or loan options that you might have.

Our goal at Bankrate is to assist you in making more informed financial decisions. Although we follow stringent guidelines, this post might mention goods from our partners. Heres an explanation for . Bankrate logo.

Bankrate was established in 1976 and has a long history of assisting consumers in making wise financial decisions. We’ve upheld this reputation for more than 40 years by assisting people in making sense of the financial decision-making process and providing them with confidence regarding their next course of action.

You can rely on Bankrate to prioritize your interests because we adhere to a rigorous editorial policy. All of the content we publish is objective, accurate, and reliable because it is written by highly qualified professionals and edited by subject matter experts.

In order to give you peace of mind when making decisions as a buyer and homeowner, our mortgage reporters and editors concentrate on the topics that matter most to consumers: the newest rates, the greatest lenders, navigating the homebuying process, refinancing your mortgage, and more. Bankrate logo.

You can rely on Bankrate to prioritize your interests because we adhere to a rigorous editorial policy. Our team of distinguished editors and reporters produces truthful and precise content to assist you in making wise financial decisions.

We value your trust. Our goal is to give readers reliable, unbiased information, and we have established editorial standards to make sure that happens. Our reporters and editors carefully verify the accuracy of the editorial content they produce, making sure you’re reading true information. We keep our editorial staff and advertisers apart with a firewall. No direct payment from our advertisers is given to our editorial staff.

The editorial staff at Bankrate writes for YOU, the reader. Providing you with the best guidance possible to enable you to make wise personal finance decisions is our aim. We adhere to stringent policies to guarantee that advertisers have no influence over our editorial content. Advertisers don’t pay our editorial staff directly, and we carefully fact-check all of our content to guarantee accuracy. Thus, you can be sure that the information you’re reading, whether it’s an article or a review, is reliable and reputable. Bankrate logo.

How we make money

You have money questions. Bankrate has answers. For more than 40 years, our professionals have assisted you in managing your finances. We always work to give customers the professional guidance and resources they need to be successful on their financial journey.

Because Bankrate adheres to strict editorial standards, you can rely on our content to be truthful and accurate. Our team of distinguished editors and reporters produces truthful and precise content to assist you in making wise financial decisions. Our editorial team produces factual, unbiased content that is unaffected by our sponsors.

By outlining our revenue streams, we are open and honest about how we are able to provide you with high-quality material, affordable prices, and practical tools.

Bankrate. com is an independent, advertising-supported publisher and comparison service. We receive payment when you click on specific links that we post on our website or when sponsored goods and services are displayed on it. Therefore, this compensation may affect the placement, order, and style of products within listing categories, with the exception of our mortgage, home equity, and other home lending products, where legal prohibitions apply. The way and location of products on this website can also be affected by other variables, like our own unique website policies and whether or not they are available in your area or within your own credit score range. Although we make an effort to present a variety of offers, Bankrate does not contain details about all financial or credit products or services.

- By refinancing your mortgage, you can use cash-out refinancing to convert equity into cash.

- Even though you are unable to withdraw the entire equity in your house, the procedure allows you to access a larger amount of money without having to sell your house.

- Your refinanced mortgage may have terms that are very different from the terms of your original loan, such as a new interest rate or a longer or shorter loan term.

Your home’s equity can be increased by paying off your mortgage, but you don’t have to wait to access that equity until you’ve paid it off in full or have sold the house. Alternatively, you can use cash-out refinancing to turn your equity into cash while still making mortgage payments.

What is a cash-out refinance?

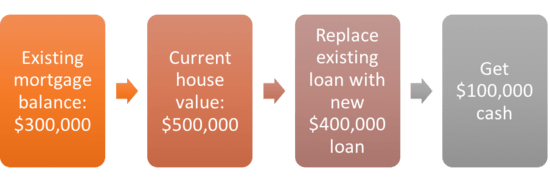

A cash-out refinance replaces your existing mortgage with a new, larger mortgage, turning the equity in your home into cash. You receive the difference between the two as a single, lump sum payment. This money can be used for anything, such as college tuition, home renovations, debt consolidation with a higher interest rate, and other necessities. Example of a mortgage cash-out refinance Let’s say your house is currently worth $400,000 but you still owe $100,000 on it. That means you have $300,000 in equity. In order to qualify for a cash-out refinance, you usually need to keep at least 20% of your home’s equity. Accordingly, in this case, you have to retain $80,000 in equity, leaving you with a maximum of $220,000 in tappable equity.

How much cash can you get with a cash-out refinance?

Mortgage lenders normally let you borrow up to 80% of the value of the house with a cash-out refinance for conventional loans. However, this threshold varies depending on the property type. For instance, you are only allowed to borrow up to 75% of the value of a multifamily home. With an FHA loan cash-out refinance, you may be able to borrow up to 80% of your house’s value. You may be able to access the full equity in your house through a VA loan cash-out.

How does a cash-out refinance work?

The procedure for a cash-out refinance is the same as for a standard refinance (also known as a rate-and-term refinance), in which you merely replace your current loan with a new one, typically with a shorter loan term, a lower interest rate, or both. The distinction is that you will receive a larger loan amount consisting of the remaining balance from the previous loan as well as money taken out of the equity in your house. The process involves:

- Determining how much cash you need: Rather than taking out a larger amount than you think you might need, it’s better to know how much you need to withdraw and for what purpose, since you will be paying interest on the new mortgage. For large-scale expenses, such as home renovations or significant debt consolidation, cash-out refinances are typically the best option.

- To find out if you qualify, a lot of cash-out refinance lenders need at least a 620 credit score and at least 20% equity in your house. Lenders with less stringent requirements may be available to you, but the cost to you may be higher.

- Looking around for the best cash-out refinance rates? To find out what you qualify for and what the current rates are, compare at least three different lenders. It might not be wise to use the equity in your house right now if you can’t get a better rate than the one you currently have.

Pros and cons of cash-out refinancing

- It is possible to reduce your interest rate, which is the main reason why most borrowers refinance. It might be advantageous for both of you if you can remove equity and obtain a lower rate than what you currently have.

- Your borrowing costs might go down because cash-out refinances frequently have cheaper interest rates than credit cards, personal loans, and home equity loans.

- You can raise your credit score: Your credit utilization may decrease if you use your equity to pay off debt. This can be a boon for your credit score.

- You can benefit from tax deductions: The interest deduction is available if the money is used for home improvements.

Cons of cash-out refinance

- Your interest rate may increase. To improve your financial status and obtain a lower rate, refinance is generally advised. Cash-out refinancing is generally not a wise choice if it raises your rate.

- Payments could last for decades: If you’re consolidating debt with a cash-out refinance, be careful not to extend repayment over decades when you could have done so much sooner and at a cheaper total cost. According to Greg McBride, chief financial analyst at Bankrate, “remember that the repayment on whatever cash you take out is being spread over 30 years, so paying off higher-cost credit card debt with a cash-out refinance may not yield the savings you’re thinking.” “It would be wiser to use the money for home upgrades.” ”.

- A cash-out refinance raises the amount owed on your mortgage, increasing your risk of losing your house. You risk losing the loan through foreclosure if you don’t make payments on it. Don’t withdraw more money than you require, and be sure to use it for something that will help rather than hurt your financial circumstances.

Is a cash-out refinance right for you?

Because your home serves as collateral in a cash-out refinance, lenders are able to take on less risk and maintain reasonably low refinance rates. That implies that one of the least expensive ways to cover major expenses is through cash-out refinancing. Many borrowers use the proceeds for the following reasons:

- Home improvement projects: For instance, you could use a cash-out refinance to build an addition or renovate your house.

- For investment purposes, you could use a cash-out refinance to buy an investment property.

- Consolidating high-interest debt: Refinance rates are typically less than those of other debt types, such as credit card debt. Instead of making multiple, more expensive monthly payments to repay the loan, you can pay off these debts with a cash-out refinance.

- Education: If the refinance rate is less than the rate for a student loan, using home equity to pay for college may make sense.

- To be qualified for a cash-out refinance, the same requirements as for your initial mortgage must be met. These prerequisites include: Credit score: usually at least 620; Debt-to-income (DTI) ratio: at least 43%; Equity: 20%, albeit occasionally less

- Closing expenses for a cash-out refinance, or any other kind of refinance, are nearly invariably lower than those associated with buying a property. The lender charges an appraisal fee and may also charge an origination fee for a cash-out refinance; these fees are typically a percentage of the loan amount. The origination fee is commensurate with the larger loan amount you receive when you cash out.

- The funds from a cash-out refinance can be used however you please. There are no limitations. Common applications, however, consist of: undertaking renovations and home improvement projects; consolidating high-interest debt; funding schooling; and providing a down payment for an investment property.

- With a cash-out refinance, you can change the rate and term and convert the equity in your house into cash. A rate-and-term refinance only modifies the length of the loan’s term and your interest rate.

- Borrowers can access the equity in their homes through both a cash-out refinance and a home equity loan, but there are some significant distinctions. Taking out a new loan for a larger amount, paying off the previous one, and receiving the difference in cash is known as cash-out refinancing. A home equity loan, in contrast, is a second mortgage. It is not a substitute for your initial mortgage and occasionally has a higher interest rate than a cash-out refinance.

- HELOC: A home equity line of credit, or HELOC, is a type of revolving credit line that functions similarly to a credit card and lets you borrow money as needed. This may be helpful if you need the funds for a remodeling project spread out over several years. The prime rate affects the variable interest rates on HELOCs. Home equity loan: Immediately following closing, you receive a lump sum payment from a home equity loan. It’s a second mortgage backed by your house, similar to a HELOC. Home equity loans have a fixed rate and immediate repayment obligations, in contrast to HELOCs. Personal loan: A personal loan is a type of shorter-term loan that can be used to finance almost anything. Like a mortgage, the interest rate on a personal loan varies greatly and is dependent on your credit history. However, the money borrowed must be repaid with monthly payments. They may require less documentation than a refinance and can be approved and funded on the same day that you apply. Reverse mortgage: With a reverse mortgage, homeowners can take out cash from their properties at any age up to 62. As long as the borrower resides in the property, maintains it, pays property taxes, and obtains homeowners insurance, the remaining amount is not due.

- Yes, in most cases. To determine how much equity you have, the mortgage lender must know the value of your house.

- A few variables could affect your payment: the rate you choose to refinance to and the amount of equity you remove. Even though you’re taking on a larger loan, you might end up with a similar payment if you refinance to a much lower rate. On the other hand, your payment will increase due to the increased loan amount if the rate is the same or higher than your existing one.

FAQ

What is the downside of a cash-out refinance?

Higher rates: Because there is more risk involved when increasing the size of your loan, cash-out refinancing loans typically have higher interest rates than conventional mortgages and rate-and-term refinances.

How does cash-out refinance work?

When you refinance with a cash-out, you take out a new mortgage that is larger than your old one, and the difference is paid to you in cash. When refinancing with cash out, you typically pay more points or a higher interest rate than when refinancing with a rate-and-term, where the mortgage amount remains the same.

How much can I refinance with cash out?

Two more calculations are needed to determine how much of your equity can be converted to cash because the majority of cash-out refinance programs won’t allow you to borrow more than 80% of the value of your home: first, multiply the value of your home by 80% ($450,000 x $200). 80 is $360,000. This is your maximum loan amount.

Do you pay taxes on cash-out refinance?

No, the proceeds from your cash-out refinance are not taxable. In essence, the cash you get from your cash-out refinance is a loan secured by the equity in your house. The money withdrawn from a cash-out refinance, home equity loan, HELOC, and other loans is not regarded as income.

Read More :

https://www.lendingtree.com/home/refinance/cash-out/

https://www.bankofamerica.com/mortgage/learn/cash-out-refinance/