What to do before applying for a mortgage

Review your credit report. At AnnualCreditReport, you can obtain free reports from the three major credit reporting bureaus: Experian, Equifax, and TransUnion. com. To avoid having your score deducted, review the report for errors and challenge anything that doesn’t seem right.

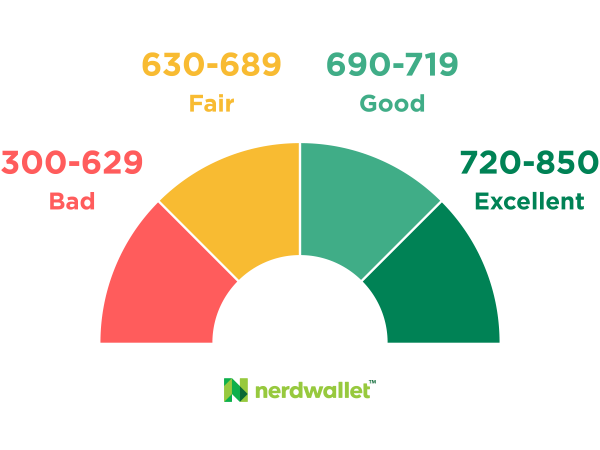

Additionally, you should be aware of where lenders will probably place your credit score. Scores in the most desirable range (720-850) are considered “excellent. From there, scores between 690 and 719 are considered “good,” 630 and 689 are considered “fair,” and 300 and 629 are considered “bad.” Your chances of getting approved for a mortgage and receiving better rate offers increase with your score.

Explore different types of mortgages. The pricing, conditions, and specifications that best suit your needs will play a major role in your decision.

For instance, if you require a mortgage with low minimum down payment requirements and flexible credit score requirements, you may want to look into Federal Housing Administration (FHA)-backed loans. You might be interested in taking advantage of an adjustable-rate mortgage’s lower introductory rate if you know you only intend to live in the house for a short period of time.

Taking into account your personal requirements as a borrower can assist you in focusing your search and locating the best kind of mortgage.

Research and compare lenders. Comparing offers and locating the best rate can be accomplished by shopping around and submitting applications to several lenders. You can start your search with NerdWallet’s list of the top mortgage lenders.

- Personal information, like your Social Security number and ID.

- Verification of income in the form of W-2s, pay stubs, or tax returns in the case of self-employment

- Federal tax returns.

- Bank statements.

- Proof of other debts and assets.

Get preapproved to borrow at a given loan amount. This is an initial application that you will complete prior to beginning your house hunt. Lenders will assess your personal data, including assets, income records, and credit report, to determine how much you might be able to borrow.

You will receive a letter from the lender outlining these outcomes. When you’re prepared to make an offer on a house, this letter can increase your chances of getting the seller to accept your offer because it demonstrates your ability to obtain financing.

Work with a real estate agent and find your home. To locate real estate agents in the area you intend to move, recommendations and internet searches can be very helpful. Interviewing several agents will help you choose one with whom you are comfortable, especially if you have particular requirements.

For instance, the house must fulfill specific requirements at the appraisal if you’re receiving an FHA loan or a loan backed by the Department of Veterans Affairs (VA). A knowledgeable realtor can help you find properties that fit these requirements.

5 steps to applying for a mortgage

After investigating lenders, obtaining a preapproval, and locating a property you wish to purchase, it’s now time to submit a mortgage application. Overall, it could take two weeks to two months to complete the entire process from application to closing.

Fill out a mortgage application

Upon completing the preapproval process, you will utilize comparable paperwork to complete an application. Applying to several lenders will provide you with a variety of rates and terms, much like with preapproval. Your credit score won’t be impacted by applying to three or four lenders any more than it would be by one application as long as all of your applications are submitted within a 45-day window and count as only one hard credit inquiry.

You can apply completely online for loans through the application portals that many lenders have on their websites. Depending on your preferred lender, you might also be able to apply over the phone or in person at a branch if you’d rather speak with someone about the process.

Even though lenders do not require it, it is a good idea to order a home inspection right away to determine the state of the property. You can learn more about the house’s condition and even decide to back out of the deal if something is discovered to be seriously flawed. This will cost around $300 to $500.

A lender is required by law to provide you with a Loan Estimate form, which is a comprehensive disclosure that includes the offered loan amount, type, interest rate, and all estimated costs associated with the mortgage, including property taxes, closing costs, and hazard insurance, within three business days of receiving your application.

Review your Loan Estimates

Applying to more than one lender has given you options. Now compare terms and costs using your Loan Estimate forms. The interest rate’s expiration dates are located in the upper right corner of the first page; determine whether the rate is “locked” or subject to change.

As soon as possible, you should lock in your rate because it needs to be completed before closing. This guarantees that from your first bill, you will know exactly what you are paying and that there won’t be any surprises.

You’ll also see a section detailing estimated closing costs. Ask the lender to explain anything you don’t understand.

A “Comparisons” section on the third page of the Loan Estimate has important data that you can utilize to contrast offers:

- Total cost in five years. This includes all fees that you will pay during the first five years of the mortgage, such as interest, principal, and mortgage insurance.

- Principal paid in five years. This represents the principal that you will have settled within the first five years.

- APR, also known as annual percentage rate. This amount includes any fees or points in addition to your interest rate. Usually, the APR is higher than your rate.

- Percent paid in interest. This shows the amount of interest that went toward the loan’s total outstanding balance. Its not the same as the interest rate.

Choose the loan estimate that best fits your needs after comparing them, then get in touch with the lender to let them know you’re prepared to proceed. They may ask for additional documentation. Additionally, you should get homeowners insurance because you’ll need it in order to get final approval.

Loan processing takes over

During this phase, your mortgage application is examined for accuracy, and every statement you made is scrutinized. Your lender will request an appraisal of the property to make sure the purchase price is justified. Prepare yourself for inquiries and requests for documentation, and act quickly to keep things going.

Any actions that could damage your credit should be avoided as they may make it more difficult to get approved for a mortgage. Avoid taking out any large loans or opening new credit lines, and make sure you pay all of your bills on schedule.

The underwriter makes a decision based on your documentation

The underwriter will use the information that the lender has now validated in your application to assess the risk of lending you money on this property.

- What is your loan-to-value ratio, or how much you are borrowing compared to the value of your house?

- Do you have enough money coming in each month to cover the payments?

- What’s your history of making payments on time?

- Is the house in good condition, has a clear title, and is the valuation accurate?

- Do you have a spotty employment history?

You might need to submit more documentation if the underwriter needs more information to decide whether to approve the loan.

Your loan is cleared to close

The lender needs to take action in this last step before you can proceed.

You receive good news from the lender with time to spare (ideally) before your closing date: “You’re cleared to close!”

Three working days prior to the date of your planned closing, the lender is required by law to send you the Closing Disclosure, another form. It shows the detailed and final costs of your mortgage.

Check to see if any of the quoted fees or amounts have changed by comparing the Closing Disclosure with your Loan Estimate. If they have, ask the lender to explain. You should lock in your rate right away if you haven’t already.

This is the time to make arrangements to pay closing costs in full, if you have chosen to do so, either by cashier’s check or wire transfer. Some borrowers include these costs in the overall loan amount. Closing costs normally range from 2% to 6% of the total loan amount. You can estimate this amount using NerdWallet’s closing cost calculator.

FAQ

Which bank is best for home loan?

|

Bank

|

Lowest Interest rate (%)

|

|

ICICI Bank

|

9.25

|

|

HDFC Bank

|

8.5

|

|

Kotak Mahindra Bank

|

8.7

|

|

Bank of Baroda

|

8.4

|

Read More :

https://www.nerdwallet.com/article/mortgages/how-to-apply-for-a-mortgage

https://www.fdic.gov/resources/consumers/consumer-news/2022-06-17.html