How Does LendingTree Get Paid? LendingTree is compensated by companies on this site and this compensation may impact how and where offers appear on this site (such as the order). LendingTree does not include all lenders, savings products, or loan options available in the marketplace.

Because many VA borrowers are exempt from VA loan limits, you may have an advantage over standard loan programs if your military service qualifies you for a VA loan. That’s particularly advantageous if you’re purchasing a home in a pricey area of the nation and don’t have a sizable down payment saved up. However, the U. S. Only if you fulfill certain requirements will the Department of Veterans Affairs (VA) support those higher loan amounts.

What are VA home loan limits?

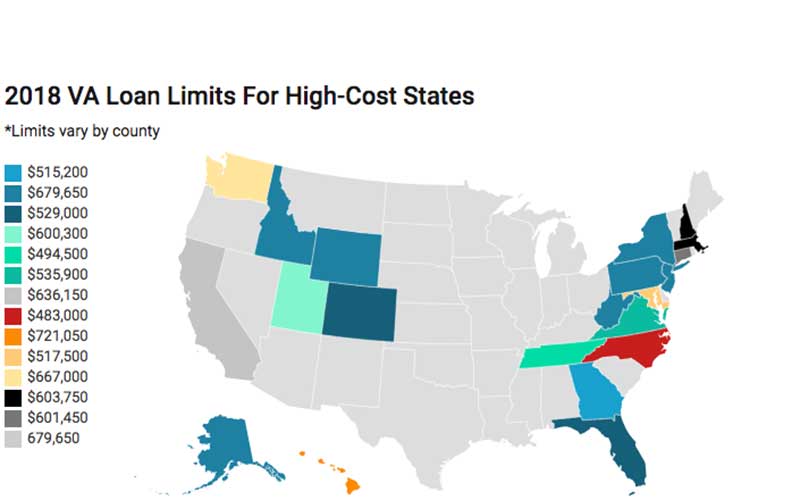

VA loan limits are ceilings on the amount of money you can borrow for a mortgage backed by the VA. Prior to 2020, all VA loan borrowers were subject to loan limits; however, this is no longer the case. The VA no longer sets a loan limit for qualified military borrowers with full entitlement, meaning they have no other active VA loans.

This means that the conforming loan limit, which sets a ceiling on the amount that borrowers of conventional loans can access, cannot be exceeded by a VA borrower who is fully eligible to buy a single-family home. Better yet, they can accomplish this without requiring a down payment. In most of the country, the conforming loan limit for 2024 is $766,550; however, for one-unit homes in high-cost areas, it rises to $1,149,825

Nonetheless, the total amount you can borrow may still be restricted by VA-approved lenders based on your credit, debt, income, and assets.

![]()

Why the VA got rid of loan limits> The Blue Water Navy Vietnam Veterans Act of 2019 eliminated loan limits for borrowers with full entitlement to give military veterans more buying power regardless of home prices. The new law also helps military borrowers avoid

You will be limited to the conforming loan limits, which are determined by the Federal Housing Finance Agency (FHFA) for every county in the nation, if you are not fully eligible and would prefer not to make a down payment.

When VA loan limits apply

Your VA home loan limit, if you don’t have full entitlement, is determined by the county in which you reside and whether you’re making a down payment. Common situations where borrowers encounter loan limits include:

- You are still making payments on a VA loan for a different residence. When active-duty VA homeowners are transferred and are unable to sell their houses before moving, this is a common occurrence.

- Although you have paid off a prior VA loan, your entitlement has not been reinstated. By giving your lender documentation proving the VA loan was fully paid, you can quickly resolve this issue.

- By refinancing your VA loan to a non-VA loan, you were able to pay it off. If your lender requires it to be sent to the VA in order to reinstate your entitlement, keep your refinance closing documents close at hand.

- You completed a deed-in-lieu of foreclosure or a short sale of your house. Additionally, following a short sale or deed-in-lieu of foreclosure, your lender may impose a waiting period before you are eligible to apply for another VA loan.

- You experienced a foreclosure due to unpaid balances on a prior VA loan. Additionally, you must wait two years following a foreclosure sale before reapplying for a VA loan.

![]() Read more about VA loan requirements and eligibility.

Read more about VA loan requirements and eligibility.

Do I have full VA entitlement?

If you have never before utilized the benefits of a VA home loan, you are eligible for a VA loan in full.

Should you have previously obtained a VA loan, you might be partially eligible. You must reinstate the entitlement that was used for that loan if you wish to regain full entitlement status. Filling out a form is all that is required to accomplish this, but it is only applicable if the loan that secures your entitlement is paid in full. For instance, if you fully paid off a previous VA loan and sold the property it was secured by, or if you had a foreclosure on a previous VA loan but paid it off, your entitlement may be reinstated.

The best way to find out how much entitlement you have now is to request a certificate of eligibility (COE) from the VA. You request a COE by logging in on the VA website. VA-approved mortgage lenders can also access your COE on your behalf.

A VA loan for a sum greater than the maximum conforming loan limits is known as a jumbo VA loan. To ensure that you can repay the larger loan amount, lenders may add additional qualifying requirements. The largest advantage of a VA jumbo loan over a regular jumbo loan is that, if you have full entitlement, you may not need a down payment, while regular jumbo loans usually require at least a 20% down payment.

It is true that you can use your VA loan entitlement as often as you like, and in certain circumstances, you can have several active VA loans open at once. When service members receive orders for a permanent change of station, it is not unusual for them to own a home in one location that was bought with a VA loan and then purchase another home in another location with another VA loan. As long as a second lender will approve their loan and they have the funds available to make a down payment when purchasing that second home with partial entitlement, they are able to do this.

Absolutely, provided that the lender offers a program that permits you to borrow up to that sum. Not every VA lender grants VA loans for sums greater than the conforming limits.

Although lenders set their own guidelines and may cap the amount of money they lend to each borrower, VA guidelines do not specify any maximum loan amounts.

The maximum VA loan amount for 20100% financing will be determined by the lender’s E2%80%99% guidelines for your area and whether you have full or partial entitlement. You are not obliged to put down money if you are fully entitled. The following procedures can be used to determine the maximum amount you can borrow without a down payment if you have partial entitlement:

- Step 1: Multiply the conforming loan limit by 0 in the county where you intend to purchase your next residence. 25. This is your maximum total guaranty.

- Step 2: Deduct from your maximum total guarantee the entitlement amount that you have already utilized. The resulting number is your total remaining VA loan entitlement.

- Step 3: Find the conforming loan limit in the county where you used your prior VA loan to buy a house, then multiply it by 0. 25. This is the amount of entitlement you’ve already used.

- Step 4: To find the maximum loan amount you can obtain without needing to make a down payment, multiply that number by four.

With poor credit, it is possible to obtain a VA home loan. Here are some tips for veterans and service members who have bad credit on how to handle the loan application process.

Though many VA lenders won’t accept a score below 620, the VA doesn’t set a minimum credit score for a VA loan.

When building a home, qualified military borrowers can apply for a VA construction loan. Learn more.

FAQ

What is the maximum you can borrow with a VA loan?

Loan caps have not applied to qualified borrowers who are fully entitled as of 2020. VA loan limits for borrowers with partial entitlements differ depending on the county in which you are purchasing a property. In the majority of the nation, the VA loan cap as of 2024 is $766,550.

What is the full VA entitlement amount?

VA Basic Entitlement: $36,000 is the basic entitlement indicated on the loan upon receipt of your Certificate of Eligibility (COE). That’s considered a full entitlement.

How many VA loans can you have in a lifetime?

The number of times you can use a VA loan to buy a house is unlimited. VA loans are intended to assist those who meet the requirements in buying a primary home. There are restrictions on using VA loans, despite their amazing benefits (such as zero down payment and government backing).

How much of my VA loan do I have left?

Step 1: Take the first VA loan amount and multiply it by zero. 25. This will indicate the amount of your entitlement that you have already utilized. Step 2:Subtract that amount from the $36,000 maximum basic entitlement. Step 3: The amount of your remaining basic entitlement is indicated by the resultant number.

Read More :

https://www.va.gov/housing-assistance/home-loans/loan-limits/

https://www.lendingtree.com/home/va/current-va-loan-limits/