What Is an Amortized Loan?

A loan that is amortized is a type of financing that is settled over a predetermined length of time. With this kind of repayment plan, the borrower makes one payment per month for the duration of the loan; the first part of the payment is applied to interest, and the remaining amount is applied to the principal amount still owed. Until the loan is repaid, a larger portion of each payment is applied to principal and a smaller portion to interest.

The minimum monthly payment is determined by loan amortization; however, an amortized loan does not prohibit the borrower from making additional payments. Generally, any additional money paid each month over the minimum debt service goes toward reducing the principal amount of the loan. This lowers the borrower’s overall interest costs during the loan’s term.

Types of Amortizing Loans

Installment loans are a type of amortizing loan where the borrower makes a monthly payment that covers the principal amount owed on the loan as well as interest. Common types of amortizing loans include:

Amortized Loans Vs. Unamortized Loans

Principal payments are dispersed over the course of the loan term with an amortized loan. This implies that interest and the loan principal are divided equally between the borrower’s monthly payments. The monthly payments on an amortized loan are greater than those on an unamortized loan of the same amount and interest rate because the borrower is paying principal and interest during the loan term.

With an unamortized loan, the borrower’s only obligation is to pay interest during the loan term. At the end of the loan term, the borrower may then be required to make a final balloon payment for the entire loan principal in certain situations. Because of this, monthly payments are typically lower. It’s crucial to budget for and save for balloon payments because they can be challenging to pay off all at once. As an alternative, a borrower may choose to make additional payments during the loan term, which will be applied to the principal amount.

Examples of common unamortized loans include:

- Interest-only loans

- Credit cards

- Home equity lines of credit

- Loans with a balloon payment, such as a mortgage

- loans with negative amortization, in which the interest paid each month is less than the interest accumulated over the same period of time

How Loan Amortization Works

Loan amortization divides a loan balance according to a set loan amount, loan term, and interest rate into a schedule of equal repayments. With the help of this loan amortization schedule, borrowers can see the total amount owed at the end of each payment period as well as the interest and principal that will be paid each month.

A loan amortization table can also help borrowers:

- Determine the total amount of interest they can avoid by making more payments.

- Use a loan payment as a guide to see how much financing they can afford.

- For tax purposes, determine the total interest paid in a given year (this includes interest paid on student loans, mortgages, and other loans with tax-deductible interest).

How to Amortize Loans

The simplest method for loan amortization is to use a template spreadsheet or online loan calculator, such as those offered by Microsoft Excel. But if you would rather amortize a loan by hand, you can use the formula that follows. You will require the entire loan amount, the length of the loan amortization period (the amount of time you have to pay the loan off), the frequency of payments (e.g., every g. , monthly or quarterly) and the interest rate.

Use this formula to determine the monthly payment on an amortized loan:

The formula is a / {[(1 r)n]-1} / [r (1 r)n] = p.

a: the total amount of the loan

r: the interest rate on a monthly basis (annual rate / number of payments annually)

n: the total number of payments (years of loan length multiplied by number of payments made annually).

Examine a $15,000 auto loan extended at a 6% interest rate and amortized over a two-year period. The calculation would be as follows:

$15,000 / {[(1+0.005)24]-1} / [0.005(1+0.005)24] = $664.81 per month

Next, multiply the total loan amount by the interest rate to determine how much of each payment will be applied to interest. Divide the result by 12 to determine the monthly interest payment amount if you plan to make payments on a monthly basis. By deducting the interest amount from your total monthly payment, you can calculate the portion of each payment that will go toward the principal.

Subtract the principal paid during that period from the outstanding balance from the previous month to determine the outstanding balance each month. Use the same calculations in the following months, but instead of starting with the initial loan amount, use the principal balance from the previous month.

In order to amortize the loan in the above example, first figure out how much interest you will pay each month by multiplying $15,000 by 6% (the percentage of the loan that is owed in this case, or $900%) and then dividing by the number of monthly payments in 2012. In this instance, the first month’s interest for the borrower will be $75 [$15,000 x 0]. 06 / 12 = $75].

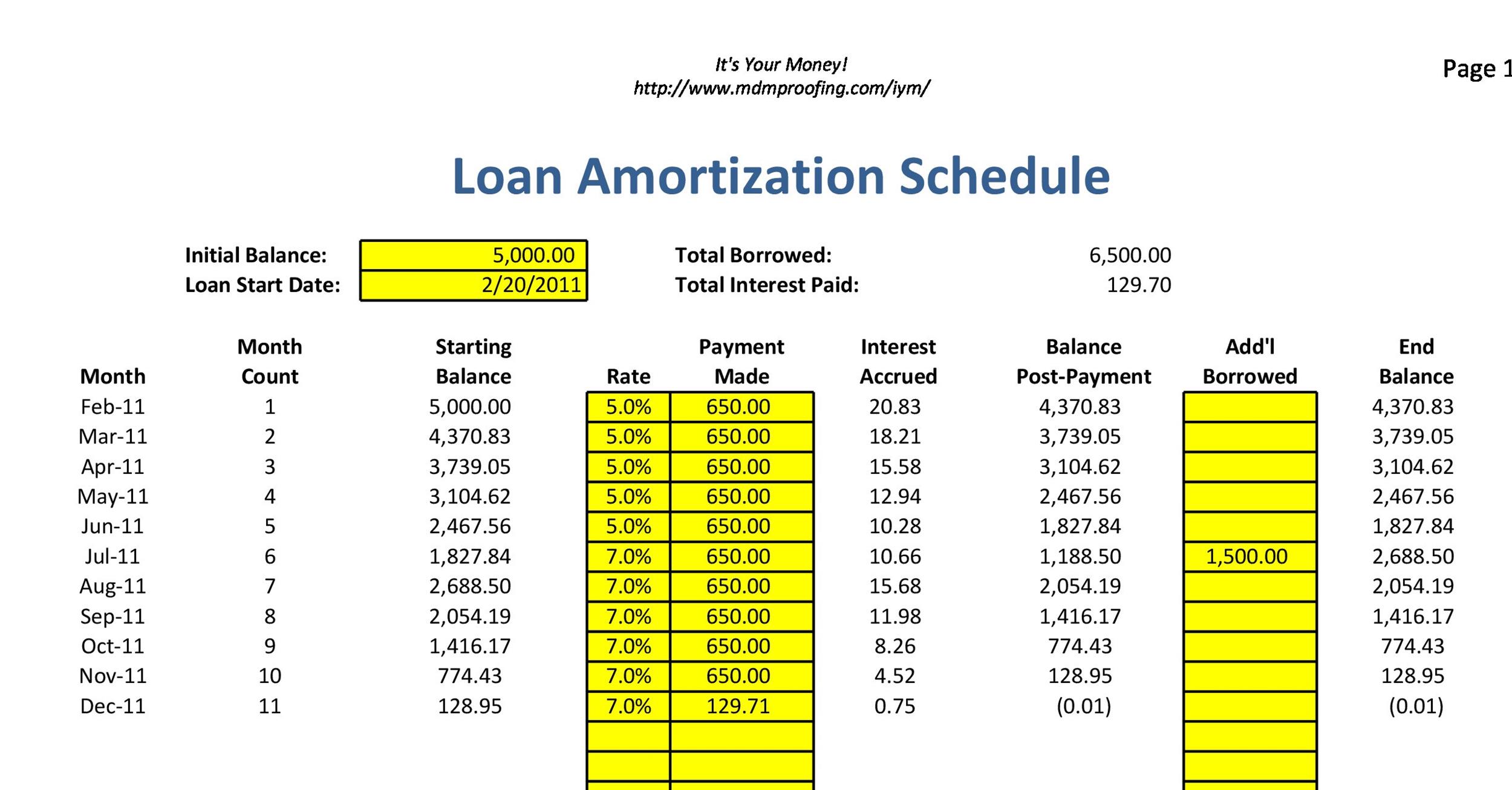

What Is an Amortization Table?

All of the scheduled loan payments, as determined by a loan amortization calculator, are listed in an amortization table. The table uses the total loan amount, interest rate, and loan term to determine how much of each monthly payment goes toward principal and interest. Although you can create your own amortization table, starting with a template that performs all of the necessary computations automatically is the simplest way to amortize a loan.

Amortization tables typically include:

- Loan details. The entire loan amount, the loan term, and the interest rate are used to calculate loan amortization. If you are using a table or amortization calculator, this data will be entered in a designated area.

- Payment frequency. The amortization table’s first column usually indicates how often you’ll be making payments, with monthly being the most typical.

- Total payment. This column includes the borrower’s total monthly payment. If you utilize a template for an amortization table, this amount will be computed automatically. Additionally, you can compute it manually or with the aid of a personal loan calculator.

- Extra payment. The amortization calculator will apply any additional funds made by the borrower above the minimum monthly payment amount to the principal and use the updated balance to determine future interest payments.

- Principal repayment. The amount of each monthly payment that goes toward paying off the loan principal is displayed in this section of the amortization table. This number increases over the life of the loan.

- Interest costs. Similar to this, an amortization table’s interest column indicates the portion of each payment that goes toward loan interest. An amortized loan’s monthly interest payments drop as time goes on.

- Outstanding balance. This column, which is derived by deducting the total principal paid over each period from the current loan balance, displays the remaining balance on the loan following each scheduled payment.

Amortization Loan Table Example

The amortization table is constructed around a $15,000 auto loan with a 6% interest rate that is paid back over a two-year period. This amortization schedule indicates that $664 would need to be paid by the borrower. 81 per month, with a $75 initial payment and a decreasing interest rate over the course of the loan. If no further payments are made, the borrower will pay $955 in total. 42 in interest over the life of the loan.

Please rate this article. Email: Please enter a working email address. Comments: We would love to hear from you. Please enter your thoughts. Send feedback to the editorial team. Something went wrong. Thank you for your feedback! Invalid email address Please try again later. Find The Best Personal Loan.

Kiah Treece is a small business owner and licensed attorney with expertise in financing and real estate. Her goal is to help people and business owners take charge of their finances by demystifying debt. lorem Is it really your intention to put your decisions on hold? The Forbes Advisor editorial staff is impartial and independent. We receive compensation from the businesses that advertise on the Forbes Advisor website in order to support our reporting efforts and keep this content available to readers for free. This compensation comes from two main sources.

FAQ

What is the meaning of loan amortization?

When a borrower takes out an amortized loan, they must make regular, scheduled payments that cover both the principal and interest. Any amount left over after the interest expense for the period is paid off by an amortized loan payment goes toward lowering the principal amount.

What is amortization in simple terms?

What Is Amortization? Over a predetermined period of time, an accounting technique called amortization is used to gradually reduce the book value of an intangible asset or loan. In terms of a loan, amortization is the process of distributing loan payments over time. When applied to an asset, amortization is similar to depreciation.

What is amortization of term loan A?

Usually, TLA tranches amortize, and the borrower must repay a portion of the TLA every year that is equivalent to between 5 0% and 20. 0% of the initial principal amount of the loan.

What does 5% amortization mean?

Assume for the purposes of this example that a lender decides to amortize a $50,000 loan at 5% annual interest over a two-year period. This implies that you will pay $875 every 60 months.

Read More :

https://www.forbes.com/advisor/personal-loans/what-is-loan-amortization/

https://www.investopedia.com/terms/a/amortized_loan.asp