What Is an Unsecured Loan?

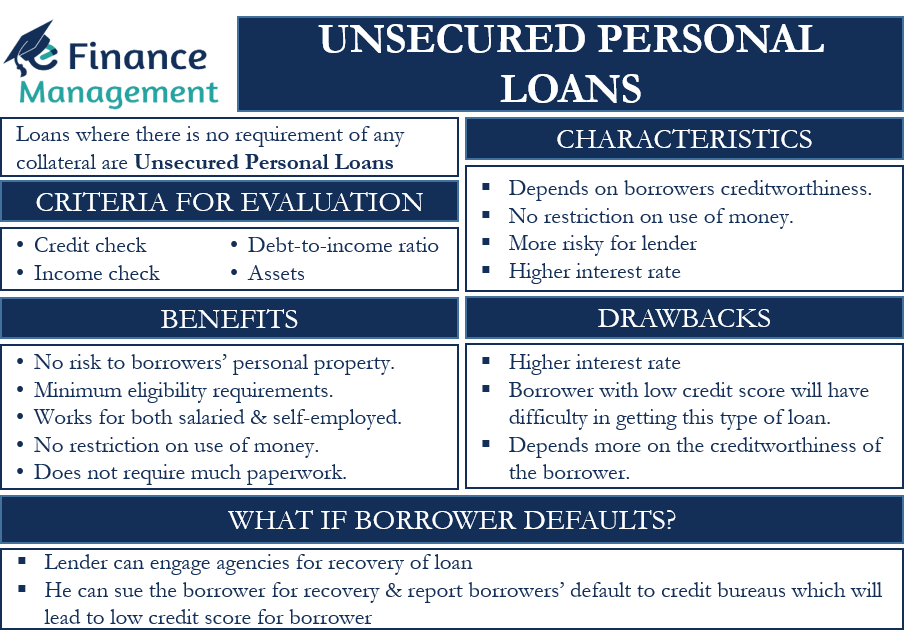

A loan that doesn’t require any kind of collateral is known as an unsecured loan. Lenders authorize unsecured loans depending on a borrower’s creditworthiness rather than their assets.

Credit cards, personal loans, and student loans are a few types of unsecured loans.

- An unsecured loan is not secured by any property or other assets; rather, it is only supported by the borrower’s creditworthiness.

- Because unsecured loans carry greater risk for lenders than secured loans, they must be approved with higher credit scores.

- unsecured loans include credit cards, personal loans, and student loans.

- If a borrower doesn’t make payments on an unsecured loan, the lender has the option of suing the borrower or hiring a collection agency to handle the debt collection.

- Based on a borrower’s creditworthiness, lenders may choose to approve or deny an unsecured loan; however, laws shield borrowers from unfair lending practices.

:max_bytes(150000):strip_icc()/unsecuredloan.asp-final-a5034e8ebf9d4622914bf0f208717774.png)

How an Unsecured Loan Works

Unsecured loans are authorized without the need for property or other assets to be used as collateral. They are also known as signature loans or personal loans. The conditions of these loans, such as their acceptance and terms, are frequently dependent on the credit score of the borrower. For unsecured loans, applicants typically need to have excellent credit scores in order to be accepted.

In contrast to a secured loan, which requires the borrower to pledge some kind of asset as collateral, an unsecured loan The assets that are pledged strengthen the lender’s “security” in granting the loan. Examples of secured loans include mortgages and car loans.

Lenders sometimes permit loan applicants with poor credit to provide a co-signer because unsecured loans have higher credit score requirements than secured loans. In the event that the borrower defaults, a co-signer assumes the legal responsibility to repay the debt. This happens when a borrower doesn’t make the principal and interest payments on a loan or debt.

Lenders take greater risk when making unsecured loans since they are not secured by collateral. These loans therefore usually have higher interest rates.

The lender may seize the collateral to cover losses if a borrower defaults on a secured loan. On the other hand, in the event of an unsecured loan default, the lender is not entitled to any collateral. However, the lender has additional options, including suing the borrower or hiring a collection agency to pursue the debt. Should the lender win in court, the borrower’s income could be withheld.

In addition, if the borrower owns a home, a lien may be put on it, or they may receive another order requiring them to repay the debt. Borrowers may experience negative effects from defaults, including decreased credit scores.

Types of Unsecured Loans

Personal loans, student loans, and the majority of credit cards are examples of unsecured loans. These loans can be either term or revolving.

A loan with a credit limit that can be used, paid back, and then used again is known as a revolving loan. Personal lines of credit and credit cards are two instances of revolving unsecured loans.

On the other hand, a term loan is one that the borrower repays over the course of its term in equal installments. Although secured loans are frequently associated with these kinds of loans, unsecured term loans are also available. Moreover, bank signature loans and credit card debt consolidation loans would be categorized as unsecured term loans.

The market for unsecured loans has expanded recently, in part due to the efforts of financial technology (fintech) companies. For instance, peer-to-peer (P2P) lending via online and mobile lenders has grown over the last ten years.

The amount of U. S. consumer revolving debt in Oct. 2023, according to the Federal Reserve.

A personal loan calculator is a great tool if you’re looking to take out an unsecured loan to pay for personal expenses because it can help you figure out what the monthly payment and total interest for the amount you want to borrow would be.

Unsecured Loan vs. Payday Loan

Alternative lenders don’t provide secured loans in the conventional sense; examples of these lenders are payday lenders and merchant cash advance providers. Unlike mortgages and auto loans, which are secured by physical assets, their loans are not. However, these lenders take other measures to secure repayment.

Payday lenders, for instance, demand that borrowers consent to an automatic withdrawal from their checking accounts or provide them with a postdated check in order to repay the loan. A lot of lenders who offer online merchant cash advances demand that the borrower use a payment processor like PayPal to process a specific portion of the borrower’s online sales. Despite being partially secured, these loans are regarded as unsecured.

Because payday loans have a reputation for having extremely high interest rates and hidden terms that charge borrowers additional fees, they may be viewed as predatory loans. In fact, some states have banned them.

Special Considerations

Although creditworthiness is a factor that lenders may consider when deciding whether to approve an unsecured loan, laws shield borrowers from unfair lending practices. For example, lenders were prohibited from using race, color, sex, religion, or any other non-creditworthiness factor when assessing loan applications, setting loan terms, or handling any other aspect of credit transactions after the Equal Credit Opportunity Act (ECOA) was passed in 1974.

Even though lending practices in the US have progressively improved equity, discrimination still happens. In order to find ways to improve the way the ECOA ensures nondiscriminatory access to credit, the Consumer Financial Protection Bureau (CFPB), which is in charge of overseeing compliance and enforcing it, released a Request for Information in July 2020. “The CFPB needs to take action to ensure lenders and other stakeholders follow the law, even though clear standards help protect African Americans and other minorities,” said Kathleen L. Kraninger, then-director of the CFPB.

What Is Considered Collateral?

Any item that can be taken as collateral to cover the loan’s value Typical collateral types include valuable goods like jewelry, cars, real estate, and other possessions.

Is a Co-Signed Loan Considered Secured?

Having a co-signer doesn’t make a loan secured, even though it might help you get approved for one. The co-signer would be required by the lender to repay the loan in the event of a default.

Can Bankruptcy Eliminate all Unsecured Loans?

Although filing for bankruptcy is a serious step, most of the time it will eliminate your unsecured debt. There is one exception, though: student loans. In an adversarial proceeding, the debtor must demonstrate that the student loans constitute an unreasonable hardship in order to have the debt forgiven. While even federal student loans are becoming easier to discharge thanks to new, streamlined adversary proceeding paperwork, private student loans used to cover living expenses have a higher chance of forgiveness.

The Bottom Line

Although unsecured loans are popular, there can be a lot of risk involved for both the borrower and the lender. Consider your ability to repay the loan and your financial situation before taking out any unsecured loans. If you take out a loan that you are unable to pay back, your wages and tax returns may be garnished, and you may have a difficult time getting back into solvency. Article Sources: Investopedia mandates that authors cite original sources to bolster their claims. These consist of government data, original reporting, white papers, and conversations with professionals in the field. When appropriate, we also cite original research from other respectable publishers. You can read more about the guidelines we adhere to when creating impartial, truthful content in our

You consent to the use of cookies on your device to improve site navigation, track user activity, and support our marketing initiatives by selecting the option to “Accept All Cookies.”

FAQ

How does an unsecured personal loan work?

You can apply for and be approved for unsecured personal loans based on your creditworthiness and your commitment to repay the loan. In addition to not needing to provide any collateral, you could be eligible for a low interest rate and flexible repayment terms.

What is bad about an unsecured loan?

Cons of Unsecured Loans: A borrower’s credit score will suffer if they miss payments or default. Default may result in legal action and subsequent wage garnishments. Lenders frequently require a higher credit score for unsecured loans than for secured loans because of the higher level of risk involved.

What is an example of a unsecured loan?

What is an unsecured loan? An unsecured loan is one that doesn’t require collateral but still has fees and interest associated with it. Unsecured loans include credit cards, personal loans, and student loans.

What is the difference between a secured loan and an unsecured loan?

Secured loans need collateral, which the lender may take back if the borrower defaults on the loan. Examples of this type of collateral include a home, automobile, or other valuable asset. Although collateral is not needed for unsecured loans, the borrower must still be deemed sufficiently creditworthy by the lender.

Read More :

https://www.investopedia.com/terms/u/unsecuredloan.asp

https://www.experian.com/blogs/ask-experian/what-is-an-unsecured-personal-loan/