We are an independent, advertising-supported comparison service. Our objective is to empower you to make confident financial decisions by giving you access to interactive tools and financial calculators, publishing original and unbiased content, and allowing you to conduct free research and information comparisons.

Issuers that Bankrate has partnerships with include American Express, Bank of America, Capital One, Chase, Citi, and Discover, among others.

Capital One Main Navigation

Have you heard the term “installment loan” but are unsure of its exact definition? An installment loan is a typical credit product. Actually, you may already own one or two of them.

Continue reading to find out more about installment loans and their operation.

Key takeaways

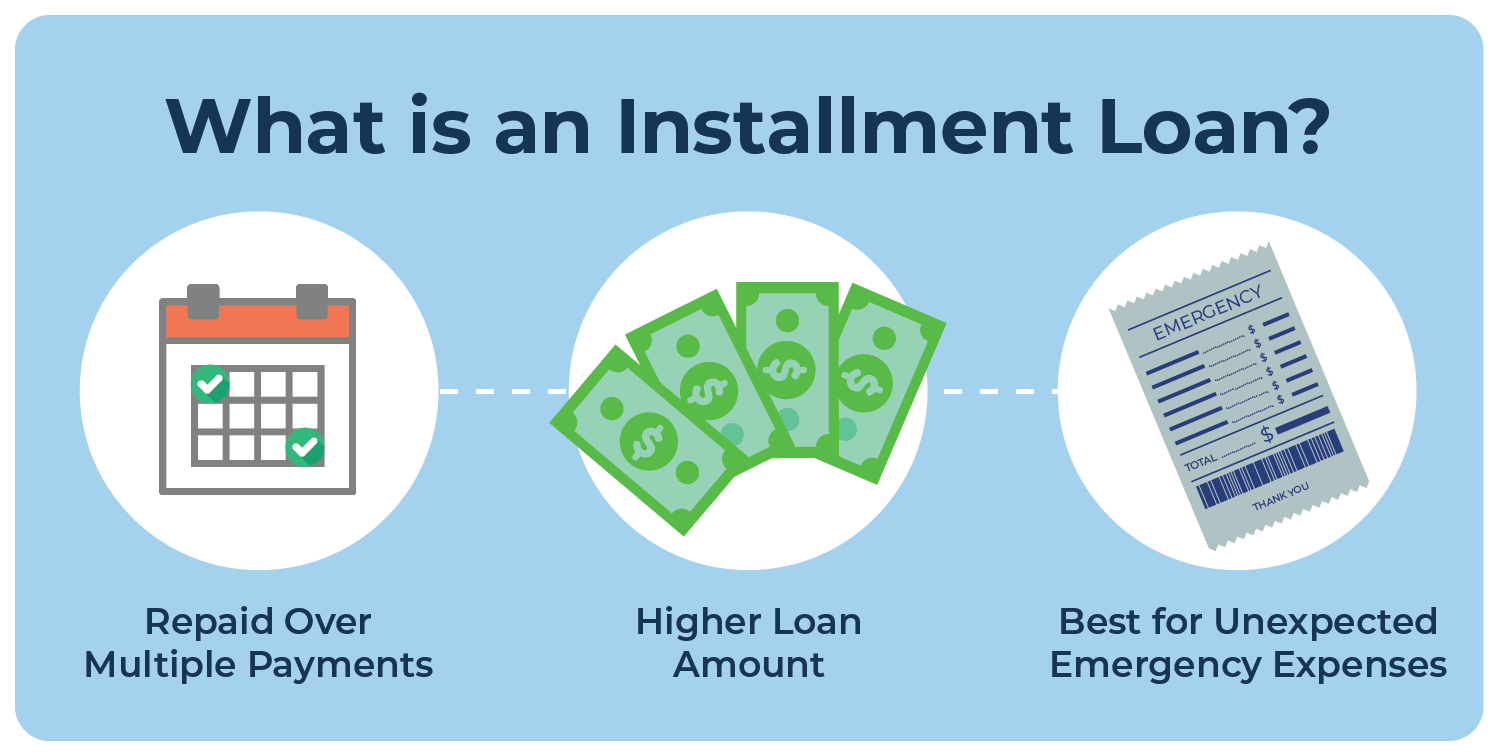

- A credit account that offers a lump amount that must be repaid over time in equal monthly installments is known as an installment loan.

- Installment loans include mortgages, student loans, auto loans, and personal loans.

- Installment loans offer advantages like fixed monthly payments as well as disadvantages like no flexibility to raise the amount if necessary.

All About Personal Loans

The way you manage your personal loan may affect your credit rating.

What is an installment loan?

Installment credit, or installment loans, are closed-ended credit accounts that you repay over a predetermined length of time. Some are intended to help with specific financial objectives, such as purchasing a home or attending college, while others can be used for a wide range of objectives.

How do installment loans work?

When you get an installment loan, the money you borrow or the item you are buying is given to you right away. Installments are the regularly scheduled payments you make to pay it off, sometimes with interest. For a predetermined number of weeks, months, or years, you usually owe the same amount on each installment. The account is permanently closed after the loan is repaid in full.

Your credit scores may affect the rate you qualify for if the installment loan you’re considering applying for has interest. If your credit is good, you might be eligible for a lower interest rate. You might still be able to get financing if your credit is average or below average, but the interest rate might be higher.

A credit card or other type of revolving account can be used as an alternative to an installment loan. Unlike installment credit, revolving credit is open-ended. This implies that as long as the account is open and in good standing, it can be used and paid down repeatedly.

Types of installment loans

Installment loans come in a variety of forms and can be either secured or unsecured. This relates to whether you require collateral, or an asset, that could be used to repay the loan in the event that you are unable to The interest rate, terms of repayment, fees, and penalties associated with each loan may vary. Shopping around is a good idea for whatever you’re looking for.

Here are some of the most common installment loans:

You are not required to use personal installment loans for any specific purchases. They can be used to pay for unforeseen expenses, make house or auto repairs, or combine outstanding debt. Most personal loans are unsecured.

Find out more about the required credit score for a personal loan.

You can use auto loans to help pay for a new or used car. An auto loan is secured by the car you buy. Auto loans typically have fixed interest rates and two to seven years as their repayment terms.

A house is purchased with a mortgage, which is backed by the property. There are lots of different types of mortgages. The most common are repaid over 15 to 30 years.

Student loans, whether federal or private, are unsecured and used to finance postsecondary education, including graduate and undergraduate degrees. In contrast to other installment loans, student loans typically do not require immediate repayment. Alternatively, you can usually wait to look for a job after graduation.

Learn more about how to apply for a student loan.

During your shopping, you may have come across a buy-now, pay-later, or BNPL loan. Some retailers offer the option at checkout. Point-of-sale financing, commonly referred to as buy-now, pay-later loans, allow you to spread out your payments over several installments rather than paying for what you buy immediately away. Depending on the merchant and the purchase, the repayment plan may last a few weeks to several years.

Payday loans are high-interest, short-term personal loans that are intended to be repaid on your next payday. The conditions and format may differ depending on the state, payday lender, and type of loan.

In exchange for a payday loan, the borrower usually gives the lender a postdated check for the full amount borrowed, plus fees. Or the borrower might authorize the lender to electronically withdraw that amount from their bank account on the due date.

Benefits and drawbacks of installment loans

There are benefits and drawbacks to every kind of credit, including installment loans. And whether it’s the best option for you will depend on the particulars of your case. Here are some points to consider:

- Capacity to pay for a substantial expense: Installment loans can provide quick access to the funds required for larger purchases.

- Regular repayments that are predictable: If you have an installment loan, you know how much each installment will cost. And this can make budgeting easier.

- Possibility of refinancing: You may be eligible to refinance if interest rates drop or if your credit score rises. For instance, refinancing could reduce your monthly mortgage payments or shorten your repayment schedule if your installment loan is a mortgage. Remember that there might be additional fees and disadvantages associated with refinancing.

- Not flexible: If you need more money, it’s unlikely that you’ll be able to increase the amount of your loan.

- Potentially lengthy commitment: The terms of repayment for certain installment loans are lengthy. This implies that the borrower must pledge to make consistent payments over an extended length of time. Additionally, make sure you review the terms and conditions of the loan. Prepayment penalties might apply if you pay off the loan early.

Do installment loans hurt your credit?

The way you use an installment loan may affect your credit scores. And, surprise! Your installment loan may be affected by your credit scores as well. Before granting you a loan, lenders consider your credit history, including your scores. Your credit score may also affect the terms and interest rates that are extended to you.

When it comes to how an installment loan could affect credit scores, it can be hard to predict. This is because there are different credit-scoring models from companies like FICO® and VantageScore®. And these companies calculate scores differently.

Your particular financial circumstances will also determine how an installment loan impacts you. Furthermore, not every installment loan is disclosed to credit bureaus. However, if your installment loan is recorded, it may benefit or detract from your credit ratings if you’re:

- Loan application: Upon submission of an application, a hard credit inquiry may be initiated. The Consumer Financial Protection Bureau (CFPB) states that these types of inquiries may have a negative impact on your credit score.

- Taking out a loan: Depending on how responsibly you use the credit and how timely you make your payments, you could improve or lower your credit scores. When you take out a new loan, your credit mix and credit utilization ratio may also alter. Furthermore, the CFPB claims that all of these variables go into determining your credit scores.

Remember that your credit scores can be impacted by additional factors. And if you want to obtain and maintain good credit scores, you’ll need to keep a watch on them all.

Installment loans in a nutshell

Installment loans are a viable option for a variety of purposes, such as debt consolidation or large purchases. Additionally, it may raise your credit score if you are able to make the payments on time and pay off the loan in full.

Starting to keep an eye on your credit is a wise first step if you’re thinking about taking out an installment loan. A copy of your credit report is available at AnnualCreditReport.com. com. Alternatively, you can use Capital One’s CreditWise to check your credit score. VantageScore 3 and your free TransUnion® credit report are available to you through CreditWise. 0 credit score anytime. And it won’t hurt your score. CreditWise is free and open to all users, not just Capital One clients. The CreditWise Simulator is another tool you can use to see how borrowing money could impact your credit score.

Remember that after you get the loan, it’s helpful to continue monitoring your credit report. It could help you know where you stand. And doing so might enable you to maintain control over your credit.

FAQ

What is an installment loan and how does it work?

Installment loans are classified as closed-end debt because they are paid back over a predetermined period of time, or loan term. Installment credit cannot be redeemed while paying off the balance, in contrast to credit cards and lines of credit, which are open-ended, revolving forms of credit.

What is the difference between an installment loan and a regular loan?

Installment loans are a type of personal loan that are paid back with a set number of scheduled payments over a mutually agreed upon time period. All that an installment loan is is a personal loan in disguise.

Do installment loans hurt your credit?

Your credit score will rise as long as you make the monthly installment payments for an installment loan on time. Your payment history accounts for 33.5 percent of your FICO score, so it’s critical that you don’t overlook a deadline.

What are the disadvantages of an installment loan?

Auto loans, mortgage loans, personal loans, and student loans are a few instances of installment loans. Installment loans have the benefits of lower interest rates and flexible terms. Installment loans have drawbacks such as default risk and collateral loss.

Read More :

https://www.capitalone.com/learn-grow/money-management/what-is-an-installment-loan/

https://www.bankrate.com/loans/personal-loans/what-is-an-installment-loan/