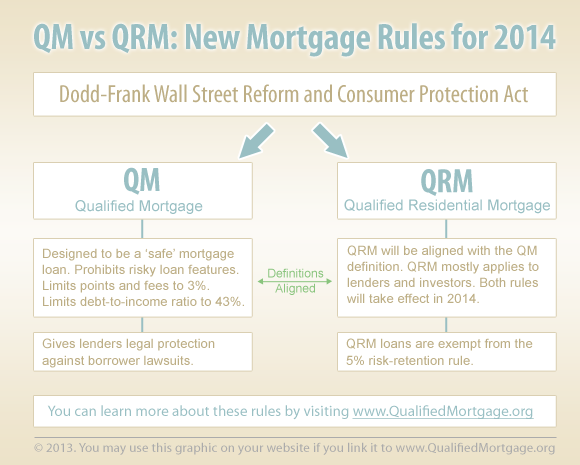

What Is A Qualified Mortgage?

A qualified mortgage loan (QM loan) satisfies every Dodd-Frank Act consumer protection requirement. Mortgage lenders are prohibited from offering mortgage products with artificially low introductory monthly payments that sharply increase when the teaser period ends. Additionally, borrowers must have a reasonable debt-to-income ratio (DTI).

What Are The QM Rules?

Examining the conditions that lenders must satisfy in order to provide you with a qualified mortgage can help you better understand what a qualified mortgage is. Qualified mortgages can’t have:

- Risky loan features: Lenders are not permitted to offer loans with risky features or artificially low monthly repayment amounts in the first few years of the loan term. These may include interest-only loans, balloon loans or negative amortization.

- A significant portion of a borrower’s income being allocated to debt: The amount of money that a borrower may allocate to debt is restricted. The percentage of your income that is applied to your debt is referred to as your debt-to-income ratio (DTI ratio), and it typically can’t exceed 2043 percent.

- Excessive upfront costs and fees: Depending on the size of the loan, there may be a limit on costs and fees, but if they exceed the threshold, the loan cannot be qualified as a mortgage.

- Loan terms longer than 30 years: Lenders are required to provide loans with a maximum 30-year repayment period. Borrowers will typically have the option of a 15- or 30-year mortgage.

A qualified mortgage also shows that your lender has complied with the “ability-to-repay” requirements, which state that they will investigate and record your employment, assets, income, credit history, and monthly expenses in an honest attempt to determine whether you can afford the loan they are offering you.

What Is A Nonqualified Mortgage?

A nonqualified mortgage, also known as a nonQM loan, is not in compliance with the Dodd-Frank Act’s consumer protection laws. These mortgages may be available to applicants with variable monthly incomes or those with special circumstances.

For instance, if your DTI is higher than 2043 percent, a lender might not be able to provide you with a qualified mortgage. Or, you might not be qualified for a mortgage if your income is inconsistent and you don’t meet Dodd-Frank’s requirements for income verification.

Instead, a lender might choose to make you an offer on a nonqualified mortgage. Even if a lender rejects your application for a mortgage, they still have to verify your income and make an assessment of your ability to repay the loan. It simply indicates that you don’t match the requirements for a mortgage that qualifies.

While loan interest rates differ from one lender to the next, you might find that a nonqualified mortgage has a higher interest rate. This is because the borrowers who apply for these loans usually have more debt and less steady incomes, which makes lenders view these loans as riskier.

Who Can Benefit From Nonqualified Mortgages?

Most borrowers end up with a qualified mortgage. But in some cases, a nonqualified mortgage is a simpler choice. For the following categories of borrowers, this might be the case:

- The self-employed

- Business owners

- Those with high levels of debt

- Those with low credit scores

- Real estate investors

- Freelance or gig-economy workers with varying incomes

Compared to qualified mortgages, nonqualified mortgages make it easier for these borrowers to purchase a property.

QM Vs. NonQM Loan FAQs

There are distinctions between qualifying for a qualified mortgage and a nonqualified mortgage, but there are also variations in the loan itself. To help you better grasp your options, here are some frequently asked questions.

What legal protections do qualified mortgage loans offer?

Dodd-Frank provided protection from legal challenges in foreclosure proceedings and other litigation to lenders issuing QM mortgages. Lenders have demonstrated that they checked your ability to repay the loan when you get a QM mortgage. This shields lenders from claims that they failed to confirm a borrower’s capacity to repay loans. But, a borrower has the right to contest the lender in court if they don’t think the lender guaranteed they would be able to repay.

Furthermore, only QMs are eligible for insurance, guarantees, or backing from FHA, VA, Fannie Mae, or Freddie Mac, making them a safer option for investors purchasing mortgage-backed securities.

How do lenders verify income for nonqualified loans?

NonQM loans give lenders more freedom to provide mortgages to borrowers who don’t meet QM loan requirements, but they still require lenders to verify the information supplied. Lenders are required to confirm and record any evidence supporting the borrower’s capacity to repay. This includes income sources. Additionally, lenders might want to confirm the borrower’s assets or anything else that assures them of their ability to repay the loan.

NonQM loans are not supported, insured, or guaranteed by Freddie Mac, Fannie Mae, the VA, or the FHA.

What is the benefit of applying for a qualified mortgage?

Qualified mortgages are the most common type of loans. You can find a loan with a lower interest rate and a monthly payment you can more easily afford by applying for a qualified mortgage.

What is the benefit of applying for a nonqualified mortgage?

Nonqualified mortgages make house loans available to borrowers who would not otherwise be eligible for one. A nonqualified loan can be the best option for you if you have poor credit, a high debt-to-income ratio, or inconsistent income that makes a conventional mortgage unfeasible.

How can I tell which type of loan is right for me?

If you are unable to obtain a qualified mortgage, request an explanation from your lender. A nonqualified mortgage can be a good option if they explain that it’s because of erratic income, higher-than-allowed DTI, a low credit score, or another problem. Still, if you have steady income, a DTI of no more than 2043 percent, and excellent credit, a qualified mortgage is a better option.

Borrowers who might not be able to obtain a qualified mortgage loan because of inconsistent income, high debt-to-income ratio, or low credit score should consider taking out a nonQM loan. While the qualifying requirements are less stringent, lenders still need to evaluate a borrower’s ability to repay and maintain standards for nonQM borrowers.

For others, though, a different loan option will be a better fit than an ineligible mortgage. Start your mortgage search online if you’re prepared to purchase a home but are unsure of the best kind for you.

Find A Mortgage Today and Lock In Your Rate! Get matched with a lender that will work for your financial situation.

With over a decade of experience in the fields of real estate, personal loans, mortgages, and personal finance, Miranda Crace is a Senior Section Editor at the Rocket Companies. Miranda is committed to increasing financial literacy and giving people the tools they need to reach their financial and home ownership objectives. After completing her studies in PR writing, film production, and film editing at Wayne State University, she graduated. Her contributions to the well-liked video series “Home Lore” and “The Red Desk,” which were shortlisted for the coveted Shorty Awards, are a testament to her creative abilities. In her free time, Miranda likes to travel, participates actively in the community of entrepreneurs, and appreciates a well-brewed cup of coffee.

Learn About Quicken Loans

LMB Mortgage Services, Inc. , (dba Quicken Loans), is not in the capacity of a broker or lender. Your submission of information to Quicken Loans does not serve as an application for a mortgage loan or a means of obtaining a lender’s pre-qualification. Your quoted rate may be higher if you are contacted by a lender or broker advertising through our network, depending on your credit score, loan-to-value ratio, debt-to-income ratio, and/or other factors. Not all states allow Quicken Loans to use its matching services. Not all credit situations may be eligible for this loan, and not all Quicken Loans network service providers provide this or other interest-only products. The companies from whom Quicken Loans and its partners may receive compensation provide the information that we offer. The choices, looks, and sequence of appearances on this website may be influenced by this compensation. Not all financial services providers or all of their goods and services are included in the data that Quicken Loans has provided. The original author or content owner, including Rocket Mortgage, has granted permission for the article’s content to appear.

Note: This website records user actions for training or quality control purposes. Input of data constitutes consent.

Rocket Mortgage, LLC is the registered trademark holder of Quicken Loans, which is used by LMB Mortgage Services, Inc. under license.

QuickenLoans.com, a LMB Mortgage Services, Inc. company NMLS #167283, www.nmlsconsumeraccess.org

FAQ

What makes a loan a QM loan?

A qualified mortgage loan (QM loan) satisfies every Dodd-Frank Act consumer protection requirement. Mortgage lenders are prohibited from offering mortgage products with artificially low introductory monthly payments that sharply increase when the teaser period ends, and borrowers must have a reasonable debt-to-income ratio (DTI).

What is the difference between QM and non-QM loans?

Differentiating factors between QM and Non-QM mortgages: QMs need traditional income documentation, such as paystubs and W2s. Non-QMs allow alternative documentation like bank statements for self-employed borrowers. DTI Requirements – QMs cap debt-to-income ratios at 43%.

What are QM requirements?

The general definition of a QM is any loan that satisfies the requirements for the product feature and has a debt-to-income ratio of no more than 23 percent.

What are the four types of a QM?

Additionally, the points and fees for all kinds of QMs cannot go above the caps on points and fees set forth in the rule. What Kinds of QMs Are There? There are four different kinds of QMs: balloon-payment, small creditor, temporary, and general.

Read More :

https://www.quickenloans.com/learn/qm-vs-non-qm-loan

https://files.consumerfinance.gov/f/201310_cfpb_qm-guide-for-lenders.pdf