This article is for educational purposes only. JPMorgan Chase Bank N. A. does not offer this type of loan. Any information described in this article may vary by lender.

Are you considering selling your house and making plans for your next move at the same time? This can be a difficult financial balance to maintain, particularly if you, like many buyers, intend to use the proceeds from the sale of your current house to purchase your new one. Fortunately, a bridge loan can make the process of purchasing a home easier.

What Is a Bridge Loan?

A bridge loan is a short-term loan that is utilized until an individual or business obtains long-term funding or settles an outstanding debt. It gives the borrower quick cash flow, enabling them to pay their existing debts. Bridge loans are typically secured by collateral, such as real estate or a company’s inventory, and have comparatively high interest rates.

These loans, also known as bridge financing or bridging loans, are frequently utilized in the real estate industry.

- A bridge loan is a type of short-term financing that is used until an individual or business obtains long-term funding or settles an outstanding debt.

- Though they are used by many different kinds of businesses, bridge loans are frequently used in real estate.

- While waiting for the sale of their current home, homeowners can use bridge loans to finance the purchase of a new residence.

:max_bytes(150000):strip_icc()/TermDefinitions_Template_bridgeloancopy-d328395628e94431ac99ef25b3f970b4.jpg)

How a Bridge Loan Works

Bridge loans, also referred to as swing loans, gap financing, or interim financing, fill the gap when funding is required but not yet accessible. Bridge loans are used by both individuals and businesses, and lenders can tailor these loans for a variety of circumstances.

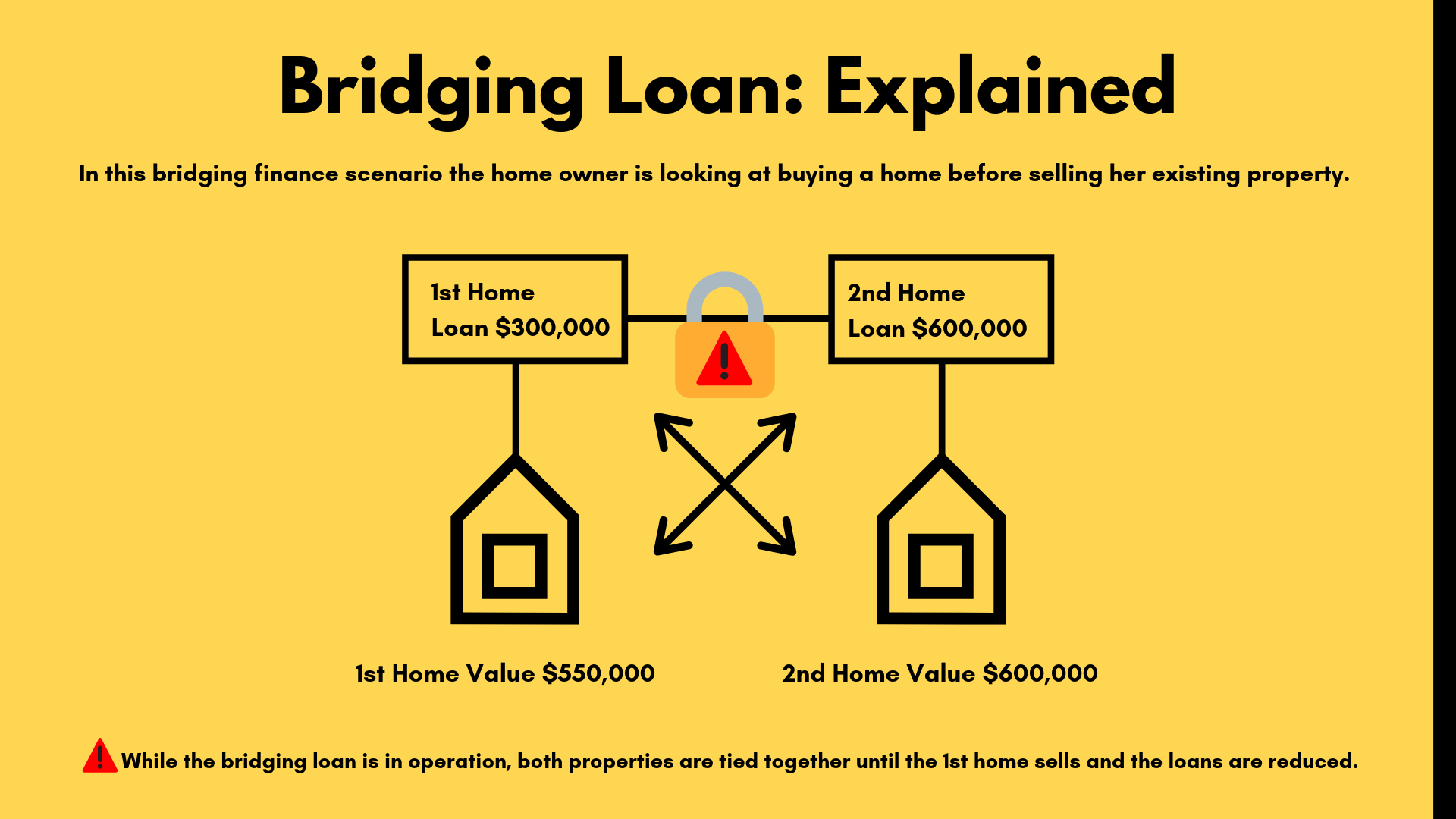

While they wait for their current home to sell, homeowners can purchase a new home with the assistance of bridge loans. While they wait for their current home to sell, borrowers utilize the equity in their current residence as a down payment for a new one.

With a bridge loan, the homeowner can extend their waiting period and, for the most part, feel more at ease. But compared to other credit options like a home equity line of credit, these loans typically have higher interest rates (HELOC)

Lenders typically only approve real estate bridge loans for borrowers with low debt-to-income (DTI) ratios and excellent credit histories. Bridge loans provide the buyer with flexibility while they wait for the sale of their previous home by combining the mortgages of two properties. Nonetheless, in the majority of cases, lenders only provide real estate bridge loans worth 80% of the total value of the two properties, which means that the borrower needs to have a sizable amount of equity in the original property or a sizable amount of cash on hand.

When businesses need money to cover expenses while they wait for long-term financing, they turn to bridge loans. Consider the following scenario: a business is raising equity and plans to close in six months. Until the funding round closes, it may choose to use a bridge loan as working capital to pay for payroll, rent, utilities, inventory costs, and other expenses.

Those who haven’t paid off their mortgage in the case of real estate bridge loans ultimately have to make two payments: one for the bridge loan and one for the mortgage until the old house is sold.

Example of a Bridge Loan

When Olayan America Corp. sought to buy the Sony Building in New York City in 2016, so it applied for an ING Capital bridge loan. The expeditious approval of the short-term loan enabled Olayan to promptly finalize the purchase of the Sony Building. Until Olayan was able to secure more stable, long-term funding, the loan assisted in partially covering the building’s purchase price.

Bridge Loans vs. Traditional Loans

Compared to traditional loans, bridge loans often have quicker application, approval, and funding processes. Nevertheless, these loans typically have short terms, high interest rates, and significant origination fees in exchange for their convenience.

Borrowers typically agree to these terms because they need quick and easy access to money. Since they are aware that the loan will have a short term and intend to pay it off quickly with low-interest, long-term financing, they are willing to pay high interest rates. In addition, most bridge loans dont have repayment penalties.

What Are the Pros of Bridge Loans?

Bridge loans provide short-term cash flow. For instance, a homeowner can buy a new house with a bridge loan before selling their current one.

What Are the Cons of Bridge Loans?

Bridge loans typically have higher interest rates than traditional loans. Additionally, you will be responsible for paying back both loans if you have a mortgage and are holding off on selling your house.

How Do I Qualify for a Bridge Loan?

You must have an outstanding credit score to qualify for a real estate bridge loan. Lenders also prefer borrowers with low debt-to-income (DTI) ratios.

The Bottom Line

Although they are frequently used in residential real estate, bridge loans are short-term financing used until an individual or business obtains permanent financing or settles an existing obligation. Many other types of businesses also use bridge loans. While they wait for their current home to sell, homeowners can use bridge loans to purchase a new property. When businesses need money to cover expenses while they wait for longer-term financing, they look for bridge loans. However, the interest rates on these loans are typically higher than those on other credit options. Article Sources: Investopedia mandates that authors cite original sources to bolster their claims. These consist of government data, original reporting, white papers, and conversations with professionals in the field. When appropriate, we also cite original research from other respectable publishers. You can read more about the guidelines we adhere to when creating impartial, truthful content in our

You consent to the use of cookies on your device to improve site navigation, track user activity, and support our marketing initiatives by selecting the option to “Accept All Cookies.”

FAQ

What does a bridging loan do?

One option to borrow a lot of money for a short period of time is through bridging loans. When purchasing real estate, they are most frequently utilized to “bridge the gap”—for instance, in situations where you must close on a deal before selling your present residence. Even though they have their uses, they carry a large risk if things don’t work out.

Why would you get a bridge loan?

A bridge loan is a type of short-term loan used to fund the down payment of a newly constructed home. If you need extra money to buy a new house before selling your current one and want to make an offer without it being contingent on your house selling first, a bridge loan can be helpful.

How much deposit do you need for a bridging loan?

Yes, a deposit of between 40% and 60% is usually required for a bridging loan. It is possible to obtain a bridging loan without a deposit (a %20100% bridging loan); however, additional assets must be in place to secure the loan against default, and stricter requirements and higher repayment amounts may be required.

Read More :

https://www.investopedia.com/terms/b/bridgeloan.asp

https://www.chase.com/personal/mortgage/education/financing-a-home/what-is-a-bridge-loan