What Is Debt Consolidation?

The process of paying off several loans with a new loan or balance transfer credit card—often at a lower interest rate—is known as debt consolidation.

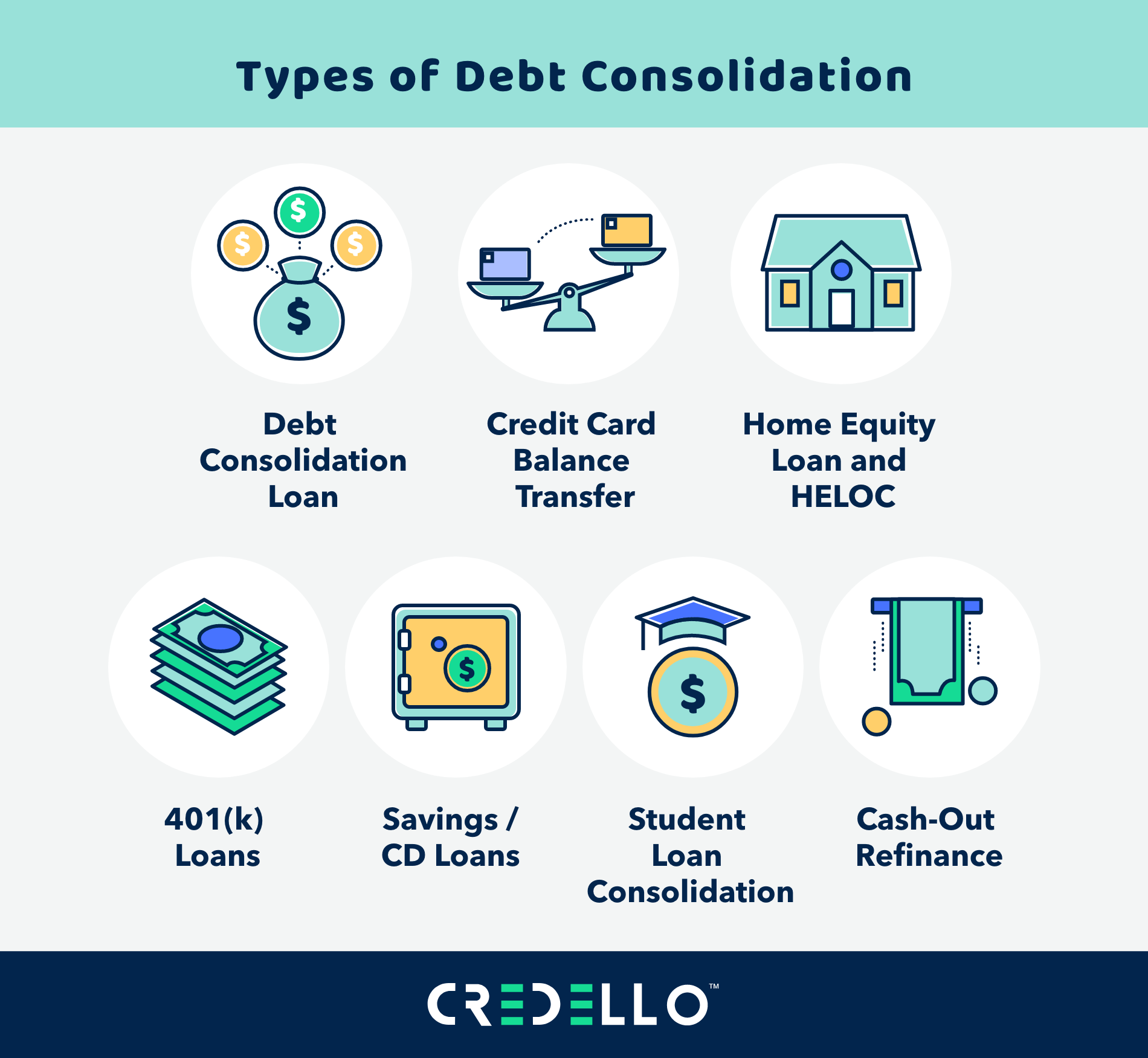

When taking out a personal loan to consolidate debt, the money earned is applied toward the repayment of each individual loan. The majority of regular personal loans can be used for debt consolidation, even though some lenders only offer specific debt consolidation loans. Similarly, certain lenders settle debts on behalf of borrowers, while others distribute the money so that borrowers can handle repayments on their own.

QUALIFYING BUYERS: With a balance transfer credit card, qualified borrowers can usually obtain an introductory APR of 200 percent for a duration ranging from six months to two years. When opening the card, the borrower can designate which balances they wish to transfer, or they can do so after the card issuer issues the card.

How Does Debt Consolidation Work?

Consolidating your debt into a single loan is how debt consolidation operates. Depending on the details of your new loan, it might enable you to pay off debt more quickly, obtain a lower monthly payment, improve your credit score, or make your financial life easier.

Debt consolidation is a three-step process:

- Take out a new loan

- Use the new loan to pay off your old debts

- Pay off the new loan

For instance, let’s say you have debt totaling $20,000. It is divided among three distinct credit cards, each with an interest rate higher than 2020%. If you were to obtain a $20,000 personal loan with a five-year term and an interest rate of 10% of 2010%, you would be able to pay off your debt more quickly and avoid paying interest.

Is Debt Consolidation a Good Idea?

In most cases, debt consolidation makes sense for borrowers who have multiple high-interest loans. That might only be possible, though, if your credit has improved since you applied for the initial loans. Consolidating your debts might not be wise if your credit score isn’t high enough to be eligible for a lower interest rate.

Additionally, if you haven’t addressed the underlying issues, such as overspending, that resulted in your current debts, you might want to reconsider debt consolidation. Paying off several credit cards with a debt consolidation loan can result in more serious financial problems later on, so it’s not a good idea to keep accruing more debt.

Pros of Debt Consolidation

A few benefits of debt consolidation include reduced interest rates and a quicker, more efficient payback schedule.

The number of payments and interest rates you have to worry about are decreased when you consolidate several outstanding debts into a single loan. Additionally, consolidation can help your credit by lowering your likelihood of missing or making a late payment. Additionally, if you’re aiming for a debt-free lifestyle, you’ll know more precisely when your debt will be settled.

May Expedite Payoff

Think about using the money you save each month to make additional payments on your debt consolidation loan if the interest rate is lower than it would be on the individual loans. This can assist you in paying off the debt sooner and ultimately save even more on interest. However, keep in mind that debt consolidation usually results in longer loan terms, so in order to benefit from this, you must make it a point to pay off your debt as soon as possible.

Could Lower Interest Rate

Even if you have mostly low-interest loans, you might be able to lower your total interest rate by consolidating debt if your credit score has increased since you applied for other loans. If you don’t consolidate with a long loan term, doing so can save you money over the course of the loan. Make sure you shop around and concentrate on lenders who provide a personal loan prequalification process in order to secure the best possible rate.

But keep in mind that some debt has higher interest rates than others. For instance, the rates on credit cards are typically higher than those on student loans. Your rate may be higher on some of your loans but lower on others if you combine several debts into a single personal loan. In this instance, concentrate on the total amount you’re saving.

May Reduce Monthly Payment

Your total monthly payment will probably go down when you consolidate your debt because subsequent payments will be spaced out over a longer loan term. Even with a lower interest rate, this could mean that you pay more over the course of the loan, so it’s not always a bad thing from a monthly budgeting perspective.

Can Improve Credit Score

Your credit score might temporarily drop if you apply for a new loan because of the hard credit inquiry. But debt consolidation can also raise your score in a variety of other ways. Paying off credit cards and other revolving lines of credit, for instance, can lower the credit utilization rate shown on your credit report. Ideally, you should have a utilization rate of less than 30%, and you can achieve that by responsibly consolidating debt. Over time, you can also raise your score by paying off the loan and maintaining a consistent, on-time payment schedule.

Cons of Debt Consolidation

It might seem like a good idea to streamline debt payoff with a debt consolidation loan or balance transfer credit card. Nevertheless, there are a few hazards and drawbacks to using this tactic.

May Come With Added Costs

Additional fees for debt consolidation loans could include origination, balance transfer, closing, and yearly fees. Before signing on the dotted line, make sure you are aware of the full cost of each debt consolidation loan when looking for a lender.

Could Raise Your Interest Rate

Consolidating your debts can be a wise move if you are eligible for a lower interest rate. But, you might be forced to pay a rate that is greater than what your present debts are if your credit score isn’t high enough to get the best deals. This could entail paying origination costs as well as additional interest throughout the loan’s term.

You May Pay More In Interest Over Time

You may still pay more in interest over the course of the new loan, even if your interest rate drops when you consolidate. The payback period for debt consolidation begins on the first day of the debt consolidation and can last up to seven years. Although the total amount you pay each month might be less than you’re used to, interest will accrue over a longer time frame.

Plan for monthly payments that are higher than the required minimum loan payment to avoid this problem. In this manner, you can profit from a debt consolidation loan without having to pay extra interest.

You Risk Missing Payments

Not only can missing payments on any loan, including a debt consolidation loan, result in additional fees, but they can also seriously harm your credit score. Examine your spending plan to make sure you can afford the additional payment in order to prevent this. Make use of autopay or any other tools that can help you prevent missing payments after you’ve consolidated your debts. Additionally, notify your lender as soon as you suspect that you might miss an upcoming payment.

Doesn’t Solve Underlying Financial Issues

While debt consolidation can make payments easier, it doesn’t change the underlying financial behaviors that caused the debts in the first place. Actually, a lot of borrowers who benefit from debt consolidation end up with more debt because they didn’t cut back on their spending and kept accruing more debt. Therefore, if you’re thinking about consolidating your debt to pay off several credit cards that are fully charged, spend some time first creating sound financial habits.

May Encourage Increased Spending

In a similar vein, using a debt consolidation loan to pay off credit cards and other lines of credit may give the impression that you have more money than you actually do. Borrowers often find themselves in a situation where they pay off debts only to discover that their balances have increased once more.

Create a budget to control your spending and ensure that you make your payments on time to avoid accruing additional debt.

When Should I Consolidate My Debt?

In certain situations, consolidating your debt can be a prudent financial move, but it’s not always the best option. Consider consolidating your debt if you have:

- A large amount of debt. If your debt is small and you can pay it off in a year or less, consolidating your debts won’t probably be worth the costs and credit check that come with getting a new loan.

- Additional plans to improve your finances. Certain debts, like medical loans, are unavoidable, but other debts are the consequence of reckless spending or other risky financial practices. Prior to consolidating your debt, assess your spending patterns and devise a strategy to gain financial stability. If not, you might accumulate even more debt than you did prior to debt consolidation.

- a high enough credit score to be eligible for a discounted interest rate You have a better chance of being approved for a debt consolidation rate that is less expensive than your current rates if your credit score has improved since you took out your previous loans. Over the course of the loan, this can help you save money on interest.

- Cash flow that comfortably covers monthly debt service. Consolidate your debt only if you can afford the additional monthly payment. Consolidation is not a good option if you are currently unable to pay your monthly debt service even though your total monthly payment may decrease.

How To Get a Debt Consolidation Loan

It can be easy to qualify for a personal loan for debt consolidation, particularly if you have a stable credit history and a high income. Here’s how to do it:

- Check your credit. Verify your credit report and score with each of the three major credit bureaus. Correct any mistakes that can have a negative impact on your credit score, and use it to determine the loans you are eligible for.

- Gather your loan application documents. This can expedite the loan application process because the majority of lenders demand the same paperwork. Among other documents, you’ll need your most recent bank statements, tax returns, W-2s, and pay stubs.

- Get a payoff estimate from your current lenders. A current debt payoff statement showing your remaining balance and any interest that has accumulated since your last payment is usually required for any debt that you plan to consolidate.

- Shop around for rates. Seek out the greatest deals that are offered to you, both online and offline. Try to prequalify to find out what rates you can get without having your credit score negatively impacted.

- Submit your application. Choose the best option and complete your loan application. In the event that the lender requests more information, reply to them right away.

- Receive the loan funds. If accepted, your lender will get in touch with you to discuss the distribution of the loan proceeds. Certain lenders settle your past debts for you, while others demand that you handle it on your own

Frequently Asked Questions (FAQs)

After you take out the loan, your lender will perform a hard credit check, so you might notice a slight decline in your credit score. Fortunately, this typically lowers your credit score by five points or less, and it has no effect on your credit score after a year. After that, as you pay back the loan, you should typically see an improvement in your credit as long as you make your payments on time.

When is debt consolidation not a good idea?

Consolidating your debts might not be wise if you are unable to get a better interest rate than you are currently paying on your current loans. Furthermore, it might not be a good idea to use your credit cards to accrue debt because you’ll end up back where you started, only with more debt.

Is it hard to get approved for debt consolidation ?

It depends on your financial situation. Getting approved for a debt consolidation loan can be simple if you have good credit, a high income, and are borrowing a small amount of money.

However, it could be challenging to get approved for a large loan if you have bad credit and little income.

How long does debt consolidation stay on your credit report?

Depending on what kind of data is submitted to the credit bureaus Your debt consolidation loan will remain on your credit report for seven years if you don’t make any payments, after which it will be automatically removed. Positive information, such as loans that you have repaid in full, will, however, remain on your credit report for ten years.

Please rate this article. Email: Please enter a working email address. Comments: We would love to hear from you. Please enter your thoughts. Send feedback to the editorial team. Something went wrong. Thank you for your feedback! Invalid email address Please try again later. Find The Best Personal Loan.

Next Up In Personal Loans

Kiah Treece is a small business owner and licensed attorney with expertise in financing and real estate. Her goal is to help people and business owners take charge of their finances by demystifying debt.

Lindsay VanSomeren is a Kirkland, Washington-based writer on personal finance. Her writing has appeared on several websites, including LendingTree, Credit Karma, and Business Insider. lorem Is it really your intention to put your decisions on hold? The Forbes Advisor editorial staff is impartial and independent. We receive compensation from the businesses that advertise on the Forbes Advisor website in order to support our reporting efforts and keep this content available to readers for free. This compensation comes from two main sources.

FAQ

Do consolidation loans hurt your credit?

While debt consolidation can result in lower monthly payments, it may also temporarily lower your credit score.

Are there any disadvantages to consolidating debt?

Additional costs could apply. Debt consolidation can be expensive. Origination fees, which are normally 1% to 10% of the total loan amount and are normally included in the loan’s annual percentage rate, can be included in debt consolidation loans.

Is a personal loan to consolidate debt worth it?

If you need to combine two or more sizable debts into a single, manageable payment, debt consolidation can be useful. When applying for a credit card or personal loan, you should try to get a lower interest rate. Since debt settlement usually follows several months of nonpayment, your credit history and score are probably in poor condition.

Is debt consolidation a good way to get out of debt?

If you’re drowning in debt, consolidating your debts could be a wise move. This is especially true if you can get an interest rate that’s less than what you’re currently paying on average for your debts.

Read More :

https://www.forbes.com/advisor/personal-loans/pros-and-cons-of-debt-consolidation/

https://www.cnn.com/cnn-underscored/money/is-debt-consolidation-a-good-idea