What are the types of bank loans for small businesses?

The following are some of the more popular kinds of business loans to take into consideration when examining possible funding options.

This loan is a conventional bank term loan option offered by a financial institution; in certain ways, it functions like a personal loan. When a company needs money for significant purchases, improvements to their operations, acquisitions, or other pressing needs, they frequently turn to this kind of loan.

These loans typically have fixed interest rates and a monthly or quarterly payment schedule required by the lender, depending on the specifics of the agreement. Additionally, the duration of these loans is set, with long-term loans lasting 10 years or potentially longer and intermediate-term loans lasting three years or less.

Consider a business line of credit similarly to how you would a credit card. Your small business can borrow from the bank up to a specific amount of money if it is approved. You only pay interest on the money you have used thus far as you accumulate debt.

This option gives you much more flexibility in how you use the money, so long as you stay within the credit limit. Small businesses that can afford it, have a good credit history, and, in certain situations, are prepared to pledge assets as collateral, should consider this option. [Read related article: What Is a Revolving Line of Credit?].

Editor’s note: Are you trying to find the ideal loan for your company? Fill out the form below, and one of our vendor partners will get in touch with you to discuss your requirements.

You need a commercial mortgage loan if your company is trying to expand and find a new location. Like a home mortgage, a commercial mortgage is backed by a lien on a commercial property.

Suppose your credit history is nonexistent or unflattering. In that instance, a bank may demand that the proprietor of the company or any principals personally guarantee the loan, agreeing to pay the debt in the event that the company fails. Commercial mortgages are much shorter than residential mortgages, which normally last 30 years.

Leasing equipment allows you to spread out the cost of a large equipment purchase over a predetermined period of time, much like renting a car. For a lease, most lessors don’t require a sizable down payment.

You have the choice to return the equipment when the lease expires. As an alternative, you can pay the remaining balance of the equipment’s worth over the term of the lease and as the item in question appreciates in value. Even though the monthly payments will be less than the total cost of buying the equipment up front, it’s crucial to remember that interest will increase the final cost.

A letter of credit is a bank’s assurance to a seller that the right payment will be made on schedule. There are two varieties of the guarantee available: buyer protection and seller protection. In the former scenario, which is typically provided for international transactions, the bank guarantees to pay the seller in the event that the buyer defaults on their payments.

Sometimes, money for this kind of letter is gathered up front from the buyer in an escrow-style arrangement. Buyer protection is provided to the seller in the form of a fine, similar to a refund. Businesses who apply for one and have the necessary collateral or credit history are given these letters by banks.

The borrower of an unsecured business loan is not required to pledge any collateral as security for the loan amount. Compared to a loan secured by collateral, the lender charges a substantially higher interest rate because it is more accommodating to the borrower than the bank. Online or alternative lenders are the most typical sources for this type of loan, though traditional banks have been known to provide unsecured loans to clients who already have a relationship with the company.

Unsecured business loans are frequently far more difficult to obtain than conventional loans since they lack any guarantees in the form of collateral. Due to the inherent risk associated with unsecured loans, they are typically offered as short-term loans in order to reduce the lender’s risk.

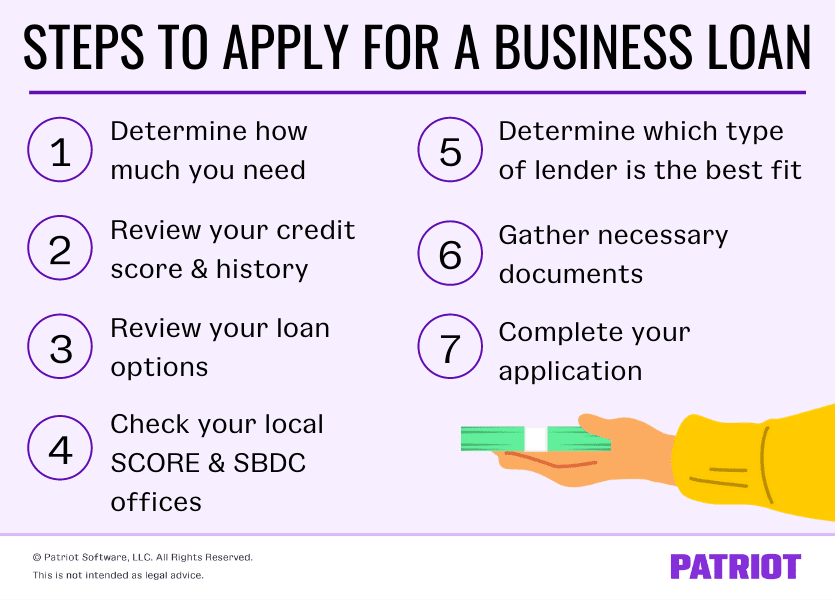

How do you get a bank loan for your business?

Follow these steps to get the funding your business needs.

Research lenders to find the right one.

Compare the top business loans side by side based on a number of criteria to find the one that best suits your requirements. Key factors include:

- Interest rate

- Rules and requirements, such as origination fees

- Qualifying criteria, such as credit scores and annual sales volume

- Collateral requirements

- How quickly you can get funding

- Additional paperwork requirements

Get your financials in order.

Find out from the bank what details, specific to the kind of loan you’re looking for and the amount of the request, it will require during the application process. In order to achieve this, you should, if at all possible, try to have three years’ worth of personal and business tax returns, along with balance sheets, year-to-date profit and loss statistics, accounts receivable aging reports, and inventory breakdowns.

You can typically obtain all of that information from your bookkeeper or CPA. But the greatest accounting programs [check out our reviews of Xero and QuickBooks] can also produce the majority of that data with equal ease.

Create a business plan.

Having your business plan written is essential if you’re a startup looking for funding. There are many free resources available if you haven’t put that in writing yet, such as SCORE, Economic Development Centers, and local Small Business Development Centers.

Estimate how much you’re going to need.

It’s also crucial to have estimates for the work or purchase ready to present to the loan officer if you need a loan for a one-time purchase or another kind of financing.

According to small business content writer Karen Axelton, “lenders want to see that you’ve carefully thought through your business goals, know how much you need to achieve them, and have a specific plan to use the money wisely.” Do the math to determine how much it will cost you to buy new machinery or open a second location. Compute the impact of loan repayments on your business’s future budget as well. ”.

Complete and submit your application (and regularly check on it).

Your final step is to complete the loan application. This process will look different for each loan. For instance, while SBA loans are notorious for their laborious, drawn-out applications, some banks advertise their speedy applications as a selling point.

After submitting your application, you should hear back from the bank within a timeframe that it has probably explicitly specified. This time frame usually lasts for at least a week, and frequently much longer. The good news is that you should have access to an online portal after completing your application, as many bank loan applications are submitted online. Typically, you can monitor the progress of your application and get in touch with your bank contact to inquire about any updates.

Review the final loan offer.

Following the approval of your loan application, the bank will draft a loan agreement tailored to your company. Make sure everything appears correct by carefully reviewing this final loan offer. Every clause in the contract pertaining to collateral, interest rate, term length, and fees should be in line with the previous discussions you had with the bank. Once everything is in order, you can sign on the dotted line.

Think carefully about the kind of loan your company will require and the kind of contract you will sign after it is authorized.

What are the requirements for getting a business loan?

Remembering a bank’s requirements is essential when applying for a business loan. Each bank has its own loan application forms. While many schools only accept online applications, some still need paper forms filled out. Depending on the type and amount of loan you’re looking for, the bank might have a preferred application procedure.

You should be aware of the requirements that a bank must meet in order for a loan application to be approved, in addition to how the bank prefers to receive them. A potential approval is based on a number of factors, so before applying, make sure to check the following:

- Credit score: A high credit score demonstrates your dependability in terms of debt repayment. Not only can a strong credit score make or break your application, but it also influences the interest rate and length of the loan that the bank extends to you.

- Objective of the loan: Certain loans have requirements regarding their utilization. For example, a mortgage is typically used for the purchase of real estate, whereas a lease is typically used to acquire equipment.

- Available collateral: If you can put up some valuable items (usually property) as collateral, some lenders will make an exception if your credit score isn’t high enough. You risk losing that collateral to the bank if you don’t follow the terms of the agreement regarding repayment; the bank will probably sell the concerned assets to offset some of its losses.

- Cash flow: A consistent source of income is what banks look for. If you don’t have a steady stream of income, traditional lenders might be hesitant to approve your loan. Many lenders don’t even consider this option until they reach a specific revenue threshold.

- Financials: Before approving a loan, the bank will want to see certain types of documents, including cash flow histories. Additionally, you must present thoroughly studied financial projections for your company.

- Business plan: Prior to considering an application, any kind of lender may request a copy of your business plan. You can find a wealth of information to assist you in beginning to draft a successful business plan for your company.

- Working capital is the amount of money that a business has available to pay for ongoing expenses. If you lack working capital, you might be viewed as a high-risk investor.

Only you know your business’s financial situation. Acquiring the necessary data can allay a lender’s worries regarding the viability of your company’s loan repayment.

What are the benefits and risks of getting a business loan?

You should weigh the benefits and drawbacks of small business bank loans listed below before deciding whether to apply.

Benefits of small business bank loans

- They come with inherent safety nets. The federal government backs banks, and the majority of their loans come with guarantees that many online and nontraditional lenders don’t. Additionally, bank loans typically have lower interest rates than loans from online lenders, so there’s less chance of you accruing unaffordable debt.

- They may offer longer terms. Bank loans are typically repayable over longer terms than other forms of business funding. This will result in smaller monthly payments, which will lessen the financial strain that comes with having loans. For instance, you would have to repay a $100,000 loan over ten years at a rate of $100,000/10 = $10,000 annually. That’s $833. 33 a month, which is significantly more affordable than repaying $100,000 over the course of a year, or $8,333 33 per month.

- They may offer flexible use terms. Certain bank loans allow you to use the money you receive however you please. When restrictions do apply, small deviations might not cause issues as long as you continue to make your payments on schedule. Naturally, you should not disregard the terms of your loan; doing so would be extremely foolish. But if you keep up timely payments and unintentionally make purchases outside the terms of your contract, bank loans usually give you more wiggle room.

Risks of small business loans

- You could choose the wrong loan. Once you’ve determined that a business loan would help your small business in the near future, you need to decide exactly what kind of loan you want to apply for. Any small business that doesn’t comply risks lost productivity, sunk costs, and other serious problems. It’s the way you waste money that you could use to find solutions that genuinely satisfy your needs.

- You could wait too long for funding. Small business bank loans may not always be helpful when you need money quickly. This is due to the fact that it may take up to six weeks for your money to be credited. By then, the opportunity for which you require funding may have already passed. Likewise, if you intend to use the loan proceeds to pay an urgent bill, there may be a significant risk associated with a slow funding disbursal.

- You could fail to repay. Getting the capital you require to expand your business does not always equate to success. You may end up in default if your growth objectives don’t generate enough income to cover your loan repayment. After that, your assets could be seized by your lender, and you might have to declare bankruptcy. All loans carry this risk, but since bank loans are frequently larger, the risk may be particularly noticeable.

Alternatives to bank loans

There are numerous loan options available to small business owners like you for financing. Every loan type has its own conditions, prerequisites, and other requirements that might make one more suitable for your financial circumstances and ability to repay than another.

Bank loans are not your only option. You can cooperate with different lenders to obtain the money you require. If a traditional loan isn’t an option for your business, you may want to look into alternative lenders. Here are three alternative lending options to consider:

- Online loans: Although the turnaround time is faster and the lenders are typically more accommodating when it comes to loan qualifications, the interest rates may be higher than with traditional loans. Lendio is one such online lender. You can submit an application through its secure interface.

- Microloans: Microloans provide a small sum of money to assist you in meeting specific business expenses. Microloans usually have a relatively low interest rate. A shorter repayment period is one of the drawbacks of microloans, and certain lenders mandate that the funds be used for particular costs, such as the purchase of equipment.

- Factoring invoices: This allows you to take out loans secured by the unpaid invoices of your clients. A factoring company will initially advance you 80–90% of the total amount of your unpaid invoices. The factoring company is then in charge of obtaining payment for the outstanding invoices. The factoring company sends you the remaining amount of your outstanding invoices, less fees, as soon as the client pays.

You can seek funding through angel investors, venture capital, and crowdfunding in addition to loans.

Terms to watch for in a business loan contract

Take into account the loan’s specifics in addition to the kind of loan you apply for. Every loan has a different interest rate and term, among other things to think about that are just as crucial as the kind of loan you choose. To ensure there are no unforeseen conditions or fees, it is crucial to read the contract in its entirety.

When applying for a bank loan, check the following:

- Rates: You must ascertain the loan rate, also referred to as the interest rate, in addition to the amount of money you want to borrow. Among other factors, the type of loan you’re looking for, the bank you’re borrowing money from, and your personal credit score all affect loan rates. If at all feasible, you should look for a business loan with a low interest rate. You may see rates that range from 3 percent to 80 percent annually percentage rate, depending on the type of loan.

- Term: This refers to how long you have to repay a business loan. Similar to the interest rate, if you can afford the payments, you should ideally have a shorter loan term. The longer your rate, the higher the total cost of your loan and the amount of interest you will pay over time.

- Banking relationship: Many organizations require you to have an established relationship with them in order to be eligible for a bank business loan. In the event that this is not the case, you will have to open an account and gradually build a working relationship with a bank.

If you are eligible, small business bank loans can assist you in financing your most audacious business objectives. Of course, it can be frightening to consider taking on a large debt load in order to support your growth. You can, however, use loans to grow your business without running the risk of losing money, as many small business owners have done.

Max Freedman contributed to this article. Interviews with sources were done for an earlier draft of this piece.

presents the b. newsletter:

Insights on business strategy and culture, right to your inbox. Part of the business. com network.

FAQ

Is it hard to get a business loan through a bank?

If your finances are not solid and your credit is not good, it may be difficult to obtain a business loan. You’ll probably need to have been in business for a number of years, have a minimum credit score in the mid-600s, and bring in $100,000 or more a year in order to be eligible for the most competitive business loans.

How much will a bank loan you to start a business?

Generally speaking, lenders will only offer loans up to 2010% to 200% of your yearly income in order to make sure you have the resources to repay them. Getting approved for a small business loan can help your company in many ways.

How do I convince a bank to give me a business loan?

Investors and lenders want to know if you have invested your own funds in the business and what value is already there. Indicate when and how your company will turn a profit. Describe the amount you plan to receive as a salary or wage from the company and whether you have any additional funding sources available.

Can I ask my bank for a business loan?

A letter that is included with your bank loan application package is called a bank loan request. The bank loan request should summarize your request and highlight the most important aspects of your company, much like a cover letter does with a resume.

Read More :

https://www.nerdwallet.com/article/small-business/how-to-apply-small-business-loan

https://www.businessnewsdaily.com/15750-get-business-loan-from-bank.html