What Is the Loan-to-Value (LTV) Ratio?

Before authorizing a mortgage, financial institutions and other lenders look at the loan-to-value (LTV) ratio as a measure of lending risk. Loan assessments with high loan-to-value ratios are typically regarded as higher-risk loans. Because of this, the loan has a higher interest rate if the mortgage is approved.

In order to reduce the risk to the lender, a borrower who has a loan with a high loan-to-value ratio might also need to get mortgage insurance. This type of insurance is called private mortgage insurance (PMI).

- In mortgage lending, the loan-to-value (LTV) ratio is frequently used to assess how much of a down payment is required and whether a lender will grant credit to a borrower.

- Lenders prefer lower LTVs, but they also necessitate higher down payments from borrowers.

- The majority of lenders provide home equity and mortgage applicants with the lowest interest rate when the loan-to-value ratio is at or below 80%.

- Mortgages become more expensive for borrowers with higher LTVs.

- Possible mortgage programs for low-income borrowers offered by Fannie Maes HomeReady and Freddie Macs Home allow an LTV ratio of 3% (the amount of the down payment) but require mortgage insurance (PMI) until the ratio reaches 80%.

How to Calculate the Loan-to-Value Ratio

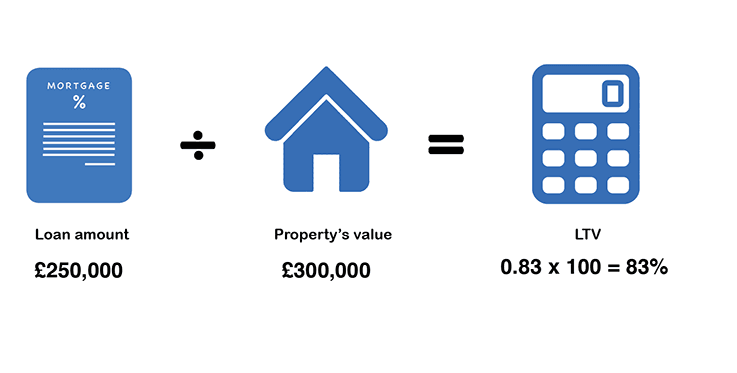

Prospective buyers can quickly determine a property’s LTV ratio. This is the formula:

Where: M A = Mortgage Amount and P V = Appraised Property Value begin{aligned}

The appraised value of the property is divided by the amount borrowed to get the LTV ratio, which is then expressed as a percentage. For instance, if you put $10,000 down and purchase a home valued at $100,000, you will borrow $90,000 in total. This results in an LTV ratio of 90% (i. e. , 90,000/100,000).

Understanding the Loan-to-Value (LTV) Ratio

An essential step in the mortgage underwriting process is figuring out an LTV ratio. It can be applied to the purchase of a house, the refinancing of an existing mortgage into a new loan, or the borrowing of funds secured by the property’s built-up equity.

When underwriting a mortgage, lenders evaluate the LTV ratio to ascertain the extent of risk they are willing to assume. Lenders believe that there is a higher likelihood of loan default when borrowers seek loans for amounts that are at or close to the appraised value (resulting in a higher LTV ratio). This is a result of the property having very little equity built up.

Because of this, if there is a foreclosure, the lender might have trouble selling the house for enough money to pay off the remaining mortgage balance while still turning a profit.

The amount of the down payment, the sales price, and the property’s appraised value are the primary variables that affect LTV ratios. A lower sales price and a larger down payment result in the lowest LTV ratio.

How LTV Is Used by Lenders

A line of credit, home equity loan, or mortgage eligibility is determined by a number of factors, not just an LTV ratio. Still, it can have a significant impact on the interest rate a borrower can obtain. The majority of lenders grant home equity and mortgage applicants the lowest interest rate when their loan-to-value ratio is at or below 80%.

Borrowers can still be approved for a mortgage even with a higher LTV ratio; however, as the LTV ratio rises, the interest rate on the loan may also increase. For instance, a borrower who has an LTV ratio of 21095 percent may be granted approval for a mortgage. That being said, their interest rate could be a full percentage point higher than the interest rate offered to a borrower with an LTV ratio of 27.55%.

A borrower might be required to obtain private mortgage insurance (PMI) if the LTV ratio is greater than 80%. This can add anywhere from 0. Five percent to one percent of the total loan amount on an annual basis In this case, for instance, PMI with a 1% interest rate on a $100,000 loan would add $1,000 more to the total amount paid annually (or $83). 33 per month). Payments from PMI are required until the LTV ratio reaches 80% or less. As you pay off your loan and your home’s value rises over time, the LTV ratio will go down.

Generally speaking, a lower loan approval rate and a lower interest rate are associated with a lower loan-to-value ratio. Furthermore, there is a decreased likelihood that you, as a borrower, will have to acquire private mortgage insurance (PMI).

Although not mandated by law, nearly all lenders practice requiring borrowers to have an 80% loan-to-value ratio to avoid the extra expense of prime mortgage insurance. Borrowers with a large investment portfolio, low debt, or high income may occasionally be exempt from this requirement.

According to general guidelines, a good loan-to-value ratio shouldn’t be higher than 80%. Anything over 80% is regarded as having a high loan-to-value ratio (LTV), which implies that borrowers may have to pay more for borrowing money, obtain private mortgage insurance, or be turned down for a loan. LTVs above 95% are often considered unacceptable.

Mortgage Example of LTV

Let’s say, for instance, that you purchase a house that is valued at $100,000. However, the owner is willing to sell it for $90,000. In the event that you make a $10,000 down payment, your loan amount is $80,000, translating into an 80% LTV ratio (i e. , 80,000/100,000). Your mortgage loan would now be $75,000 if you were to increase your down payment to $15,000. This would make your LTV ratio 75% (i. e. , 75,000/100,000).

Variations on LTV Ratio Rules

Regarding the LTV ratio requirements, different loan types may have different regulations.

FHA Loans

FHA loans are mortgages designed for low-to-moderate-income borrowers. They are insured by the Federal Housing Administration and issued by lenders who have been approved by the FHA.

Compared to many conventional loans, FHA loans have lower minimum down payments and credit requirements. FHA loans permit a maximum initial LTV ratio of 96. 5%, but they require a monthly mortgage insurance premium (MIP) that is applicable for the duration of the loan (regardless of how low the LTV ratio eventually falls).

A lot of people choose to refinance their FHA loans in order to waive the MIPP requirement once their LTV ratio reaches 80%.

VA and USDA Loans

VA and USDA loans are available to current and former military personnel as well as those living in rural areas. Private mortgage insurance is not required, even though the loan-to-value ratio can reach as high as 20100%. However, both VA and USDA loans do have additional fees.

Fannie Mae and Freddie Mac

Home Possible mortgage programs offered by Fannie Maes and Freddie Macs to low-income borrowers allow an LTV ratio of 2097 percent. Nevertheless, they demand mortgage insurance until the ratio drops to 80%.

There are simplified refinancing options for FHA, VA, and USDA loans. Due to the waiver of appraisal requirements, the loan amount is unaffected by the home’s LTV ratio. There are other options available for borrowers who have an LTV ratio of more than 10% of the total. These borrowers are also referred to as being underwater or upside down. Fannie Maes High Loan-to-Value Refinance Option and Freddie Macs Enhanced Relief Refinance Option are also available.

Upfront fees on Fannie Mae and Freddie Mac home loans changed in May 2023. Fees were increased for homebuyers with higher credit scores, such as 740 or higher, while they were decreased for homebuyers with lower credit scores, such as those below 640. Another change: Your down payment will influence what your fee is. The higher your down payment, the lower your fees, though it will still depend on your credit score. Fannie Mae provides the Loan-Level Price Adjustments on its website.

LTV vs. Combined LTV (CLTV)

The combined loan-to-value (CLTV) ratio is the ratio of all secured loans on a property to the value of a property, whereas the LTV ratio examines the impact of a single mortgage loan when buying a property. This covers any second mortgages, home equity loans, credit lines, other liens, and home equity loans in addition to the primary mortgage utilized in LTV.

When a potential homeowner has multiple loans, such as a mortgage plus a home equity loan or line of credit, or two or more mortgages, lenders utilize the CLTV ratio to assess the buyer’s default risk (HELOC) Overall, lenders are generally willing to lend money to borrowers with high credit ratings at CLTV ratios of 80% and above. Since CLTV is a more comprehensive metric, primary lenders are typically more lenient with it.

Lets look a little closer at the difference. The LTV ratio solely takes into account a home’s principal mortgage balance. Consequently, LTV%20=%2050% if the primary mortgage balance is $100,000 and the home’s value is $200,000.

But let’s look at the scenario where it also has a $30,000 second mortgage and a $20,000 home equity loan. The combined debt to value now stands at ($100,000%20 %20$30,000%20 %20$20,000%20/%20$200,000)%20=%2075%; a significantly higher ratio

These combined factors are particularly crucial in the event that the mortgagee defaults and faces foreclosure.

What Is a Good LTV?

The threshold that most lenders use to determine what constitutes a good loan-to-value (LTV) ratio is 80%. Anything below this value is even better. Keep in mind that when the LTV rises above 80%, borrowing costs may increase or borrowers may not be approved for loans.

What Are Disadvantages of Loan-to-Value?

The primary disadvantage of an LTV’s data is that it only accounts for a homeowner’s primary mortgage; other debts, like a second mortgage or home equity loan, are not factored into the computations. As a result, the CLTV is a more comprehensive indicator of a borrower’s capacity to pay back a mortgage.

What Does a 70% LTV Mean?

A 70% (0. The loan-to-value (LTV) ratio of 70) signifies that the loan amount is equivalent to 70% of the asset’s value. In the event of a mortgage, this would imply that the borrower has made a 20% down payment and is financing the remaining amount. As an example, a $500,000 property with a 1%700% loan-to-value ratio would require a $150,000 down payment and a $350,000 mortgage.

How Is LTV Calculated?

Simply divide the loan amount by the value of the asset or collateral being borrowed against to find the loan-to-value (LTV). This would be the mortgage amount divided by the value of the property in the case of a mortgage. Article Sources: Investopedia mandates that authors cite original sources to bolster their claims. These consist of government data, original reporting, white papers, and conversations with professionals in the field. When appropriate, we also cite original research from other respectable publishers. You can read more about the guidelines we adhere to when creating impartial, truthful content in our

You consent to the use of cookies on your device to improve site navigation, track user activity, and support our marketing initiatives by selecting the option to “Accept All Cookies.”

FAQ

What is the formula for loan value?

Loan-to-value, or LTV, is computed by taking the total loan amount and dividing it by the asset or collateral that is being borrowed against. This would be the mortgage amount divided by the value of the property in the case of a mortgage.

How do you calculate 80% LTV?

The amount of the mortgage divided by the property’s value is known as the loan-to-value ratio. It is expressed as a percentage. If you obtain a mortgage of $80,000 to purchase a $100,000 home, the loan-to-value ratio is 80% since you obtained a loan covering 80% of the $100,000 home’s worth.

How do you calculate LTV value?

What is the LTV formula? An LTV ratio calculator will calculate your loan’s LTV ratio using the following formula: LTV= principal amount / market value of your property.

How do you calculate loan to cost value?

Loan-to-cost analysis (LTC) contrasts a commercial real estate project’s financing amount with its actual cost. LTC is computed by dividing the loan amount by the cost of construction.

Read More :

https://www.bankofamerica.com/mortgage/learn/how-to-calculate-home-equity/

https://www.investopedia.com/terms/l/loantovalue.asp