An employer-sponsored retirement plan called a 401(k) enables employees to set aside money from their paychecks. You can borrow from a 401(k) plan before you retire, but it can also help you live comfortably in retirement. What you should know about 401(k) loans, including how they operate, how much you can borrow, and what happens if you change jobs

401(k) Loan Basics

Since 401(k) loans don’t involve a lender or a credit report review, they are technically not considered loans. More precisely, they are defined as the capacity to access a portion of your own retirement plan funds, typically up to $50,000 or 20%50% of the assets, whichever is less than 20%E2%80%94 on a tax-free basis. After that, you’ll have to pay back the funds you took out in accordance with regulations meant to return your 401(k) plan to something like how it was before the transaction.

Another confusing concept in these transactions is the term interest. Since the participant repays any interest accrued on the outstanding loan balance into their own 401(k) account, technically speaking, this is also a transfer of funds from one pocket to another rather than an expense or loss associated with borrowing. Therefore, the impact of a 401(k) loan on the growth of your retirement savings may be negligible, neutral, or even positive. However, it will typically be less expensive than the real interest paid on a bank or consumer loan.

Loans are permitted under 401(k) plans, but the employer sponsoring the plan is not obligated to make them available to plan participants.

When a 401(k) Loan Makes Sense

One of the first places you should definitely look for funding when you have an urgent need for cash is a loan from your 401(k) plan. Lets define short-term as being roughly a year or less. Let’s use a significant one-time demand for funds or a lump-sum cash payment as our definition of “serious liquidity need.”

“Let’s face it, people need money sometimes in the real world,” Kathryn B. Hauer, CFP, MBA, is a financial planner with Wilson David Investment Advisors and the author of “Financial Advice for Blue Collar America.” “Borrowing from your 401(k)—or even a more reasonable personal loan—can be a more prudent financial move than taking out a payday, pawn, or title loan with cripplingly high interest rates. It will cost you less in the long run. “.

The reason your 401(k) is a desirable source for short-term loans is that it may be the easiest, quickest, and least expensive way to obtain the money you require. Unless the loan limits and repayment guidelines are broken, receiving a loan from your 401(k) is not taxable and has no effect on your credit score.

A short-term loan should generally not significantly impact your progress toward retirement savings if you repay it on time. In certain instances, it may even have a favorable effect. Lets dig a little deeper to explain why.

:max_bytes(150000):strip_icc()/dotdash_Final_4_Reasons_to_Borrow_From_Your_401k_Apr_2020-011-476fff8e835242c39a99ce76c52e8764.jpg)

Of course, there are other strategies to avoid ever having to take out a 401(k) loan.

“While ones circumstances in taking a 401(k) loan may vary, a way to avoid the downsides of taking one in the first place is preemptive,” said Mike Loo, vice president of wealth management at Trilogy Financial. “If you are able to take the time to preplan, set financial goals for yourself, and commit to saving some of your money both often and early, you may find that you have the funds available to you in an account other than your 401(k), thereby preventing the need to take a 401(k) loan.”

Examine every available loan option and contrast it with a 401(k) loan. Then, before you make your final choice, consider the main justifications for borrowing in the first place.

Top 4 Reasons to Borrow from Your 401(k)

Requesting a loan in the majority of 401(k) plans is simple and fast; no extensive applications or credit checks are needed. Usually, it has no effect on your credit score or results in a credit inquiry.

With just a few clicks on a website, you can request a loan through many 401(k) plans and receive the funds within a few days in complete privacy. Debit cards are one innovation that some plans are now implementing, allowing for the instantaneous, small-dollar lending of multiple loans.

Repayment Flexibility

For the majority of 401(k) loans, you can repay the plan loan sooner without incurring a prepayment penalty, even though regulations specify an amortizing five-year repayment schedule. The majority of plans enable easy loan repayment through payroll deductions; however, you must use after-tax funds rather than the pretax ones that fund your plan. Similar to a standard bank loan statement, your plan statements display credits to your loan account and your remaining principal balance.

Cost Advantage

You can use your own 401(k) funds to meet short-term liquidity needs at no cost—possibly the exception of a small loan origination or administration fee. Heres how it usually works:

You designate which investment account or accounts you would like to borrow money from, and those investments are liquidated during the loan period. As a result, you forfeit any gains that those investments might have generated for a brief time. Additionally, you are selling these investments for less money when the market is down than it otherwise would be. The benefit is that you won’t lose any more money on this investment.

The interest rate on a comparable consumer loan less any lost investment gains on the borrowed principal is the cost advantage of a 401(k) loan. Here is a simple formula:

Cost Advantage is equal to Lost Investment Earnings – Cost of Consumer Loan Interest.

For example, suppose you obtain a personal loan from a bank or obtain a cash advance from a credit card at an interest rate of 8%. Your 401(k) portfolio is generating a 5% return. The cost advantage that you would receive by borrowing from the 401(k) plan would be 3% (8% – 5% = 203).

A plan loan may be alluring whenever you can predict that the cost advantage will be positive. Remember that since consumer loan interest is paid back with after-tax dollars, this calculation does not account for any potential tax benefit.

Retirement Savings Can Benefit

Repayments for loans made to your 401(k) account are typically reinvested in the investments in your portfolio. The amount that you repay to the account in excess of what you borrowed is known as “interest.” If any lost investment earnings equal the “interest” paid in, the loan has no (i.e., neutral) effect on your retirement because interest payments balance earnings opportunities dollar for dollar.

You can actually accelerate your retirement savings if you take out a 401(k) loan and the interest paid is greater than any lost investment earnings. But be aware that this will correspondingly lower your non-retirement personal savings.

401(k) Loans and Their Impact on Your Portfolio

After going over the previous point, let’s talk about another criticism of 401(k) loans: If you take money out, it will significantly hurt your portfolio’s performance and the growth of your retirement savings. Thats not necessarily true. First of all, as was already mentioned, you do return the money, and you do so quite quickly. Considering the average 401(k)’s long-term horizon, this is a relatively short (and financially insignificant) period of time.

The second issue with the reasoning that has a negative impact on investments is that it frequently assumes a constant rate of return over time, even though the stock market doesn’t operate that way, as recent events have made abundantly evident. There will be ups and downs in a growth-oriented, equities-heavy portfolio, particularly in the near run.

The true effect of short-term loans on your retirement progress if your 401(k) is invested in stocks will depend on the state of the market at the time. In strong up markets, the effect should be somewhat negative; in sideways or down markets, it may even be neutral or even positive.

The bad news is that you should wait to take out a loan until you believe the stock market is weakening or vulnerable, which is typically the case during recessions. Interestingly, a lot of people discover that they require money to remain liquid during these times.

The Employee Benefit Research Institute found that in 2020, the percentage of 401(k) participants with outstanding plan loans was as of this writing (latest information available).

Debunking 401(k) Loan Myths With Facts

Two other prevalent criticisms of 401(k) loans are that they are not tax-efficient and that they cause participants great stress when they are unable to repay them before they retire or quit their jobs. Lets confront these myths with facts:

Tax Inefficiency

The argument is that because 401(k) loans must be repaid with after-tax money, double taxation applies to loan repayment, making them inefficient from a tax standpoint. This treatment only applies to the interest portion of the repayment. When weighed against the costs of other options for obtaining short-term liquidity, the cost of double taxing loan interest is frequently relatively minimal.

This is a hypothetical scenario that is all too frequently very real: Let’s say Jane steadily increases her retirement savings by putting aside 7% of her salary in her 401(k). But she’ll soon have to take out a $10,000 loan to cover her college expenses. She expects to be able to pay this back with her pay in about a year. She is in a combined federal and state tax bracket as of 2020. Here are three ways she can tap the cash:

- Borrow from her 401(k) at an “interest rate” of 4%. The amount she will pay in double taxes on the interest is $80% (20000 loan x 4% interest x 2020 tax rate).

- Take out a loan from the bank at a real interest rate of 8%. Her interest cost will be $800.

- Put a year’s worth of 401(k) plan deferrals on hold and use the proceeds to cover her college expenses. In this scenario, she will pay more in current income tax, forfeit any employer-matching contributions, and lose actual retirement savings progress. The cost could easily be $1,000 or more.

Interest on 401(k) loans is double taxed; this is only a significant expense if substantial sums are borrowed and paid back over a number of years. Even so, it is typically less expensive than using bank loans, consumer loans, or a pause in plan deferrals to obtain comparable sums of money.

Leaving Work With an Unpaid Loan

Let’s say you take out a plan loan and then you get laid off. You will have to repay the loan in full. If you do not pay the entire amount owed, the loan balance will be deemed taxable and you may be subject to a federal tax penalty of 10% of the unpaid balance if you are under the age of twenty-five percent (2059) C2%BD. Although tax law is accurately described by this scenario, reality is not always reflected in it.

Many people, particularly those who are tight for cash, decide to take a portion of their 401(k) funds as taxable distributions upon retirement or separation from employment. Making this decision and having an outstanding loan balance have comparable tax ramifications.

Before taking a distribution, those who wish to avoid unfavorable tax outcomes can use other resources to pay back their 401(k) loans. If they do, the entire balance of the plan may be eligible for a rollover or tax-advantaged transfer. In the event that an unpaid loan balance is included in the participant’s taxable income and is later repaid, the 2010 penalty will not be applied.

Taking out 401(k) loans while working and not intending or being able to pay them back on time is a more serious issue. The unpaid loan balance in this instance is handled similarly to a hardship withdrawal, which could have a detrimental effect on plan participation rights in addition to having negative tax repercussions.

401(k) Loans to Purchase a Home

Loans from 401(k) plans must be repaid over a maximum of five years on an amortizing basis, which means that they must be paid back according to a set schedule of regular installments, unless they are utilized to buy a primary residence. Longer payback periods are allowed for these particular loans. However, the IRS is silent on the duration, so you’ll need to discuss this with your plan administrator.

Taking out a mortgage loan might be more appealing than completely financing a home purchase with a 401(k) loan. Like most forms of mortgages, plan loans do not allow tax deductions for interest payments. Furthermore, while taking out a loan and paying it back within five years is acceptable under standard 401(k) terms, repaying a loan over an extended period of time can have a substantial negative impact on your ability to reach retirement.

On the other hand, if you require quick money to pay for a down payment or closing costs for a house, a 401(k) loan might be a good option. It also won’t have an impact on your eligibility for a mortgage. The 401(k) loan has no impact on your debt-to-income ratio or credit score, two important variables that influence lenders, because it isn’t technically considered a debt because you are withdrawing your own funds.

Should you require a substantial amount to buy a home and wish to utilize 401(k) funds, you may want to think about taking out a hardship withdrawal in addition to or instead of the loan. However, you will have to pay income tax on the withdrawal, and if the total exceeds $10,000, you will also be subject to a 2010 penalty.

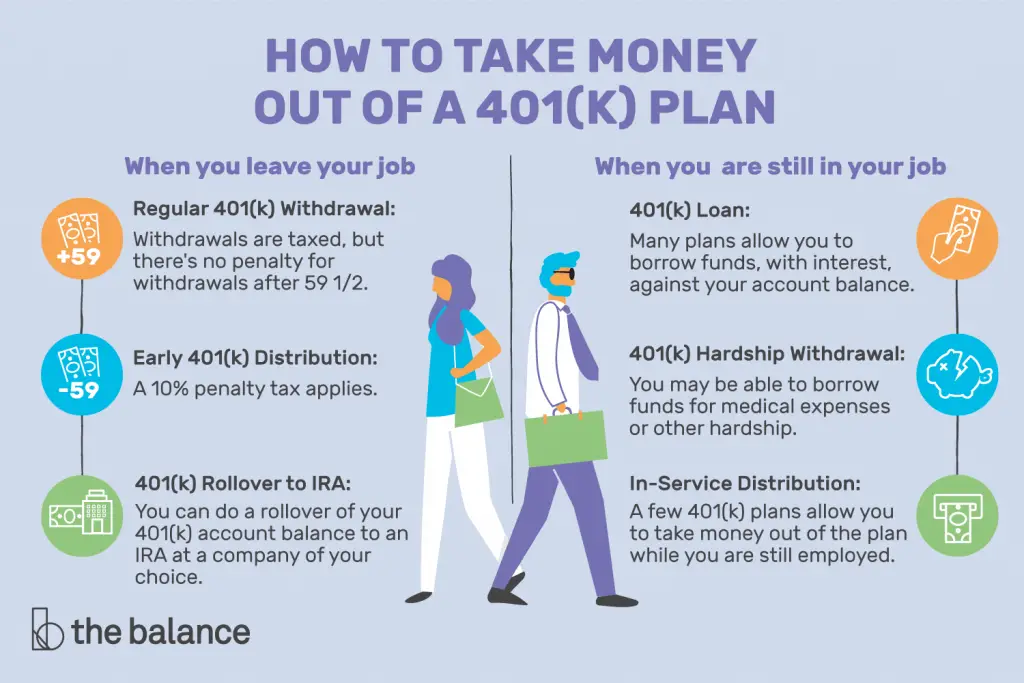

How Much Can I Borrow from My 401(k)?

Generally speaking, you are able to borrow up to $50,000 or ten percent of the assets in your 401(k) account, whichever is less, and within a twelve-month period. You are still able to borrow up to $10,000 even if the balance in your vested account is less than $10,000. Remember that not all plans offer 401(k) loans because plan sponsors are not obligated to offer them.

Is Taking a 401(k) Loan a Good Idea?

In certain situations, taking out a 401(k) loan could be a smart move. If you require money now, say to cover an unforeseen bill, a 401(k) loan may be able to help. The most important factors are keeping the loan short-term—a year or less—and repaying it on time.

How Do I Repay a 401(k) Loan?

Loan repayments are normally made through payroll deductions, just like 401(k) contributions. A 401(k) loan is typically due back in five years, unless the money is used to buy a house. In that case, you have longer. Additionally, you can repay the loan earlier without incurring early payment penalties.

The Bottom Line

Arguments that 401(k) loans are detrimental to retirement accounts frequently have two flaws: they assume that the 401(k) portfolio will always have strong stock market returns, and they neglect to account for the interest costs associated with borrowing comparable amounts from a bank or other consumer loans (like piling up credit card debt).

Don’t be afraid to take advantage of a worthwhile liquidity option included in your 401(k) plan. These transactions can be the easiest, most convenient, and least expensive way to obtain cash when you lend yourself the proper sums of money for the appropriate temporary purposes. You should always have a clear repayment plan in place before taking out any loans so that you can pay them back on time or early. Article Sources: Investopedia mandates that authors cite original sources to bolster their claims. These consist of government data, original reporting, white papers, and conversations with professionals in the field. When appropriate, we also cite original research from other respectable publishers. You can read more about the guidelines we adhere to when creating impartial, truthful content in our

When you visit the site, Dotdash Meredith and its partners may store or retrieve information on your browser, mostly in the form of cookies. Cookies collect information about your preferences and your devices and are used to make the site work as you expect it to, to understand how you interact with the site, and to show advertisements that are targeted to your interests. You can find out more about our use, change your default settings, and withdraw your consent at any time with effect for the future by visiting Cookies Settings, which can also be found in the footer of the site.

FAQ

How much of your 401k can you borrow?

Loan amounts: $50,000 or half of the vested account balance, whichever is lower, is available for borrowing. That being said, the borrower may withdraw up to $10,000 if the account balance is less than $10,000. Loan terms: A 401(k) loan usually has a five-year repayment period.

How much can you withdraw from a 401k?

Generally speaking, a qualified distribution is one you get after you turn 59 1/2. Once you reach this age, you can take as much money out of the account as you’d like. You pay taxes at your regular income tax rate on qualified distributions from a 401(k) after the age of 59 1/2.

Is it a good idea to take a loan from your 401k?

While taking out a loan from your 401(k) isn’t the best option, there are some benefits, particularly when weighed against taking an early withdrawal. Avoid taxes or penalties. With a loan, you can escape the fines and taxes associated with making an early withdrawal.

What is the 12 month rule for 401k loan?

The following are the guidelines for taking out a 401(k) loan: there is a 2012 month lookback period, which allows you to borrow up to 2050 percent of the total amount you have vested in all of your accounts over the last 12 months, reduced by the highest amount of outstanding balance during this lookback period.

Read More :

https://www.investopedia.com/articles/retirement/08/borrow-from-401k-loan.asp

https://www.fool.com/retirement/plans/401k/loan/