What is a home equity line of credit?

A second mortgage that allows you to access cash based on the value of your house is called a home equity line of credit, or HELOC. (If you own your home outright, it can also be your primary mortgage.) You take out a loan against your equity, which is the market value of your house less the principal mortgage balance. Generally, you can borrow up to 85% of your equity, though the exact amount will depend on the lender.

Similar to a credit card, you can take out and repay all or part of a home equity line of credit each month. But HELOCs aren’t meant for small purchases like a credit card

Taking out a loan against the equity in your house will typically result in the best interest rate when you’re shopping around.

Key takeaways

- With a HELOC, you can take out a loan against the value of your house, ideally to pay for investments that will increase your wealth, like renovations.

- The majority of Home Equity Loan providers allow you to borrow up to 85% of the value of your house (less the amount you owe), however some have higher or lower limits.

- A home equity line of credit usually allows you to take out cash for ten years, with only interest to be paid back. After that, you have twenty more years to repay the principal amount plus interest at a variable rate.

- Lenders typically require you to have a credit score above 20620, a debt-to-income ratio below 2040%, and equity of at least 2015 in order for you to be qualified.

Today’s HELOC rates

Lender-to-lender rates differ, and the annual percentage rate, or APR, you are given is primarily determined by things like:

- Your credit score.

- Your existing debt.

- The amount you wish to borrow.

The prime rate, the lowest credit rate that lenders are willing to offer their most desirable borrowers, is the base rate that most HELOC rates are indexed to.

To determine a rate offer, lenders take into account the borrower’s profile and add a margin to the prime rate. For example, if a lender applies a margin of 1. 5% to a prime rate of 8. 5%, that borrower’s rate will be 10%.

Sometimes a lender may add a negative margin. In order to entice borrowers, a lender might offer this as part of an introductory offer before later on in the loan term switching to a positive margin.

|

Current prime rate |

Prime rate last month |

Prime rate in the past year — low |

Prime rate in the past year — high |

|---|---|---|---|

|

8.50%. |

8.50%. |

7.50%. |

8.50%. |

Most HELOCs have adjustable interest rates. This implies that the interest rate on your HELOC will fluctuate in tandem with changes in the benchmark interest rate. But since a HELOC is backed by the value of your house, the interest rate is usually more akin to a mortgage rate than it is to that of a credit card or personal loan.

Getting the best HELOC rate

To find the best HELOC rate, compare offers from at least three lenders. Check with your bank or mortgage provider; they may provide discounts to current clients. Additionally, pay attention to promotional offers such as initial rates that end at the end of a specific term.

You may want to look for lenders that provide a fixed-rate option before opening a HELOC. This can protect your loan from rising interest rates and make long-term financial planning a little easier by allowing you to lock in your APR when you take out equity.

How does a HELOC work?

With a HELOC, you can take out loans against the equity in your house, pay them back, and keep borrowing. Because your home serves as the security for a HELOC, interest rates are usually competitive. They are risky because you could lose your house if you are unable to make your payments.

There are two phases of a HELOC:

- During the draw period, you can withdraw funds from the account up to the authorized maximum. While principal payments are optional, interest payments are required. This period typically lasts 10 years.

- The repayment period is the time frame during which you are unable to take out new loans and must pay back principal as well as interest. When considering the draw period, the monthly payments may increase significantly due to the addition of principal. The repayment period varies in length, but it typically lasts 20 years.

PNC: NMLS#446303

How do I access a HELOC?

There are several ways for you to take money out of this account. You have access to it through an online transfer, an ATM or point of sale using your bank card (just like you would with a debit card), or, if the lender issues checks, you can write checks from the account.

How much does a HELOC cost?

Before taking out a HELOC, there are additional expenses to take into account in addition to interest.

- Closing expenses, which are typically between 2% and 5% of the loan amount Although some lenders waive closing costs entirely, keep in mind that this may be conditional on keeping the line open for a predetermined period of time.

- Annual fees. For HELOC clients, some lenders impose annual fees, which are typically in the neighborhood of $50.

HELOC requirements

While lender requirements may differ, the following are the standard requirements to obtain a HELOC:

- A debt-to-income ratio thats 40% or less.

- A credit score of 620 or higher.

- A house valued at at least 2015% more than what you owe

How to get a home equity line of credit

Obtaining a HELOC is comparable to applying for a mortgage to be purchased or refinanced. You’ll present some of the same records and prove your creditworthiness. Here are the steps you’ll follow:

- Determine how much you need to borrow by calculating your existing equity, which is the current value of your home less what you owe.

- To ensure a smooth application process, gather the required paperwork in advance, including W-2s, recent pay stubs, mortgage statements, and personal identification.

- Shop around multiple lenders and apply for the HELOC.

- Read your disclosure documents carefully and ask the lender questions. Make sure the HELOC will fit your needs. For instance, is getting the best rate on the HELOC contingent upon opening a second bank account or requiring you to borrow thousands of dollars up front (often referred to as an initial draw)?

- Be advised that while the underwriting procedure is not as drawn out as it was for your mortgage, it can still take weeks.

- Wait for the loan closing to sign the documents and open the credit line.

Don’t assume that your home’s current value is equal to the amount you paid at closing. Your lender might request an appraisal during underwriting to verify the value of the property. You’ll also have more equity if local home prices have increased during the time you’ve owned your house because there will be a bigger difference between the increased value of the property and the amount still owed on your mortgage.

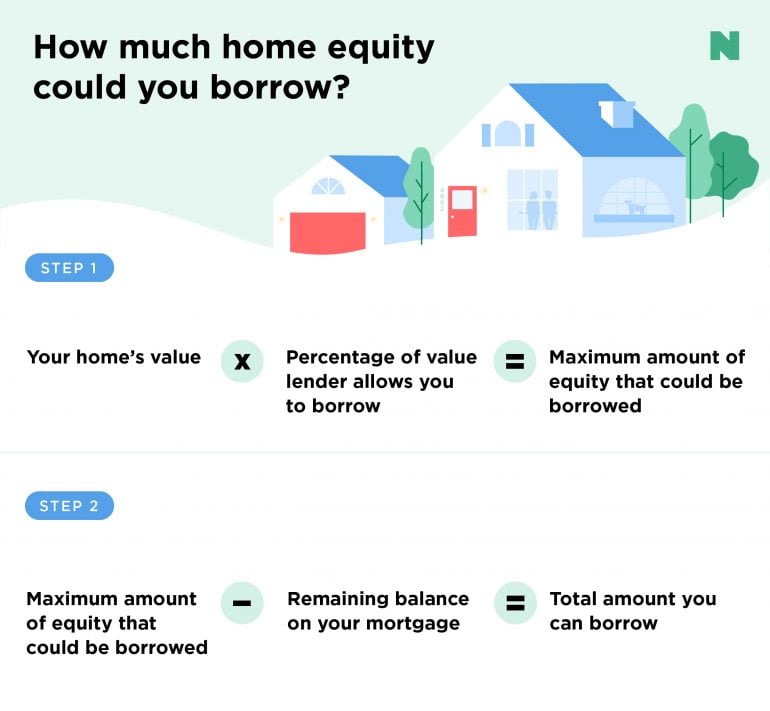

How much can you borrow with a HELOC?

The value of your house, the portion of its value that the lender will let you borrow against, and the amount of your mortgage debt will all affect the maximum amount of your home equity line of credit. You can estimate how much you might be able to borrow with a HELOC by performing two quick calculations.

Your current home’s value multiplied by the lender’s allowable percentage of value equals the maximum amount of equity you could borrow.

The total amount you can borrow is equal to the maximum amount of equity that could be borrowed minus the remaining balance on your mortgage.

Let’s say your home is valued at $300,000 and you owe $200,000 on your first mortgage. Your lender will give you access to up to 85% of the value of your home. Multiplying $300,000 (the value of the home) by the percentage that the lender will let you borrow (85%, or $200) 85) provides you with a maximum equity loan amount of $255,000. To find the total amount you can borrow with a HELOC, deduct the amount you still owe on your mortgage ($200,000). This will leave you with $55,000.

Alternatively, use the HELOC calculator below to estimate how much you might be able to borrow without having to do the math.

Is getting a HELOC a good idea?

A home equity line of credit may or may not be a good choice for you depending on your financial situation and goals.

Pros

- Home improvement and repair with a HELOC can raise the value of your property.

- A HELOC might offer you a better rate than an unsecured loan.

- According to the IRS, if you use the money from your HELOC to purchase, build, or significantly improve your home and the total amount of your mortgage and HELOC does not exceed specified loan limits, the interest on your HELOC may be tax deductible.

Cons

- Refinancing becomes more likely if you are unable to make loan payments.

- If your income is erratic or you fear that you won’t be able to make your payments in the event that interest rates rise, a HELOC is not advised.

- If you intend to move shortly, it might not be the best option. A HELOC’s extended borrowing and payment period is one of its key advantages; however, you must pay it off in full at the time of sale.

A home equity line of credit (HELOC) might not be the best option if you don’t plan to borrow a large amount of money (in which case the costs might not be justified and you should think about getting a low interest credit card instead), or if you plan to use the money for necessities, one-time purchases, or expenses that don’t contribute to your personal wealth (such as a vacation or new car).

Is it better to get a home equity loan or line of credit?

That depends on your financial situation and needs. With a home equity line of credit (HELOC), you can access the value of your house as needed, just like with a revolving line of credit. A home equity loan has a lump-sum withdrawal that is repaid in installments, much like a traditional loan.

While home equity loans are typically issued with a fixed interest rate, HELOCs typically have variable interest rates. If interest rates rise in the future, this can protect you from a payment shock. Determine which choice is best for your financing needs by consulting with your lender.

What to do if you can’t keep up with your HELOC payments

Due to the adjustable rate found in most HELOCs, it is possible that your payments will be higher than you had anticipated. It’s critical to take quick action if you anticipate a problem because the lender may foreclose on your property if you are unable to repay the money you have taken out. Speak with the lender to learn about your options, and think about refinancing to reduce your interest rate or modify the terms of your payments.

An example of a second mortgage that allows you to borrow against your home equity is a home equity line of credit, or HELOC. You use the funds from the HELOC as needed and then gradually repay it, much like with a credit card.

The two stages of a HELOC are referred to as the draw period and the repayment period. You borrow money as needed during the draw period, and the required monthly payments typically only cover interest. You will repay the principal and interest during the repayment period, after which you will no longer be able to borrow money.

Using a HELOC, you can borrow money as needed rather than all at once. Even with a large credit limit overall, interest is only charged on the money you really use. Because HELOC rates are typically adjustable, they change in tandem with the market.

If you used the loan for home improvements, you might be eligible to claim a tax deduction on the interest paid on your HELOC. In order to take advantage of this deduction, you must itemize your deductions because the IRS sets annual limits that differ based on whether you are filing jointly, as a head of household, or as an individual.

When it comes to HELOCs, some credit bureaus treat them more like installment loans than like revolving credit lines. This indicates that borrowing 10% of your HEC limit may not have the same detrimental effects as using up all of your credit card. A new HELOC on your record will probably temporarily lower your credit score, just like any other line of credit. But, if you borrow sensibly—that is, by paying your bills on time and not using the entire credit limit—your HELOC might eventually raise your credit score. What is a HELOC?.

One kind of credit is a home equity line of credit, or HELOC.

that lets you borrow against your home equity. You use the funds from the HELOC as needed and then gradually repay it, much like with a credit card. How is a HELOC paid back?.

comprises two stages, referred to as the repayment period and the draw period. You borrow money as needed during the draw period, and the required monthly payments typically only cover interest. You will repay the principal and interest during the repayment period, after which you will no longer be able to borrow money. How does a HELOC work?.

Using a HELOC, you can borrow money as needed rather than all at once. Even with a large credit limit overall, interest is only charged on the money you really use. HELOCs generally have adjustable interest rates, so.

on your home equity loan interest if the loan was utilized for remodeling In order to take advantage of this deduction, you must itemize your deductions because the IRS sets annual limits that differ based on whether you are filing jointly, as a head of household, or as an individual. How does a HELOC affect your credit score?.

When it comes to HELOCs, some credit bureaus treat them more like installment loans than like revolving credit lines. This indicates that borrowing 10% of your HEC limit may not have the same detrimental effects as using up all of your credit card. A new HELOC on your record will probably temporarily lower your credit score, just like any other line of credit. But, if you borrow sensibly—that is, by paying your bills on time and not using the entire credit limit—your HELOC might eventually raise your credit score.

ADDITIONAL INFORMATION FOR CANADIAN READERS: What is a home equity credit line?

PNC: NMLS#446303

FAQ

What is the downside to a HELOC?

The most evident drawback of a HELOC is that you have to secure the loan with your home as collateral. The variable interest rate feature of HELOCs is less beneficial in the current rising interest rate environment because the Federal Reserve has signaled that it will need to maintain higher interest rates for an extended period of time.

What is the monthly payment on a $50000 HELOC?

Finding the monthly payment for a $50,000 loan with an eight percent interest rate 75% is the average rate for a fixed home equity loan from 2010 to the present. As of September 25, 2020, the monthly payment would be $626. 63. Additionally, this monthly payment would remain the same for the duration of the loan because the rate is fixed.

How do payments work on a HELOC?

During the draw period, HELOCs enable you to make interest-only payments; subsequently, you can make principal and interest payments. On a home equity line of credit, additional principal payments lower your monthly payments and accelerate loan payoff.

Is a HELOC a good idea right now?

Reduced interest rates: Although the average interest rate on home loans has increased significantly since 2022, home equity loan interest rates are still typically lower than those on credit cards and personal loans. A HELOC can be a less expensive way to finance home improvements or debt consolidation if you qualify for the best rates.

Read More :

https://www.nerdwallet.com/article/mortgages/heloc-home-equity-line-of-credit

https://www.usbank.com/home-loans/home-equity/how-home-equity-lines-of-credit-work.html