3 Steps to Calculate Your Student Loan Interest

It’s actually not too difficult to figure out how much interest lenders charge for a particular billing cycle. All you have to do is follow these three steps:

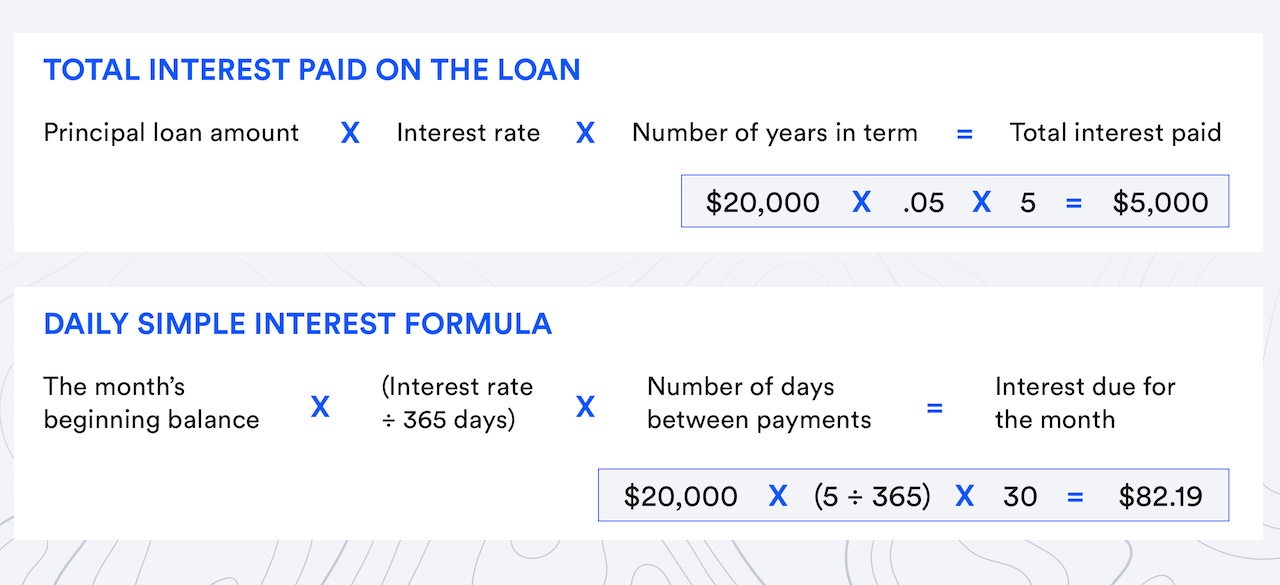

Step 1: Calculate the Daily Interest Rate

To calculate the amount of interest that accrues daily, first take your loan’s annual interest rate and divide it by 365.

Let’s say you owe $10,000 on a loan that has 5% annual interest. You’d divide that 5% rate by 365: 0. 05 ÷ 365 = 0. 000137 to arrive at a daily interest rate of 0. 000137.

Step 2: Identify Your Daily Interest Charge

Next, multiply the outstanding principal by the daily interest rate you calculated in Step 1. Again, let’s use $10,000 as an example for this calculation: 0 000137 x $10,000 = $1. 37.

This $1. The daily interest that you are assessed is 37, which means that you are being charged $1. 37 in interest on a daily basis.

Step Convert It Into a Monthly Amount

The daily interest amount must then be multiplied by the total number of days in your billing cycle. Assuming a 30-day cycle in this instance, the monthly interest payment would be $41. 10 ($1. 37 x 30). The total for a year would be $493. 20.

This is how interest is calculated from the time your loan is disbursed, unless you have a federal loan that is subsidized. If so, interest is not assessed until the end of your six-month grace period following your graduation from school.

You have the option to pay off any accumulated interest on unsubsidized loans while you’re still enrolled in classes. If not, after graduation the accumulated interest is capitalized, that is, added to the principal amount.

Remember that even though your payments may stop during a forbearance, interest will still accrue and will eventually be added to your principal amount if you request and are granted one. A forbearance is essentially a pause on repaying your loan, usually for about 12 months. Only if you have an unsubsidized or PLUS loan from the government will interest continue to accrue if you experience economic hardship (which includes unemployment) and enter into deferment.

:max_bytes(150000):strip_icc()/how-to-calculate-student-loan-interest-4772208_final-39fc8391e4e2462e91d1632c7f8abe72.png)

Student loan payments have been suspended and interest rates have been fixed at 200 percent during the COVID-19 pandemic. As of February 2023, this is still the case, but it could alter when either of the following two events occurs first: either 60 days after the department is given permission to carry out the student loan forgiveness plan or the lawsuit is settled, or 60 days after June 30, 2023.

Simple vs. Compound Interest

The computation above illustrates how to determine interest payments using a basic daily interest formula; this is how the U S. Department of Education does it on federal student loans. By using this approach, interest is only paid as a percentage of the principal amount.

Nevertheless, some private loans use compound interest, which multiplies the daily interest by the outstanding principal plus any accrued unpaid interest rather than the principal amount at the start of the billing cycle.

Thus, you are not applying the daily interest rate of zero on day two of the billing cycle. 000137, in our instance—to the $10,000 in principal that you had at the beginning of the month. The daily rate is being multiplied by the principal and the interest that was accumulated the day before, or $1. 37. The banks benefit from it since, as you can expect, they are able to collect higher interest when they compound it in this manner.

A fixed interest rate for the duration of the loan is also assumed in the calculation above, which is what a federal loan would have. Nevertheless, depending on the state of the market, the rates on some private loans are variable. You would need to use the current interest rate on your loan to calculate your monthly interest payment for a specific month.

Compound interest, which is applied to certain private loans, is calculated by multiplying the daily interest rate by the monthly principal amount plus any accrued but unpaid interest.

Student Loan Amortization

If you have a fixed-rate loan, whether from a private lender or the Federal Direct Loan Program, you might notice that even though the interest rate and remaining principal decrease each month, your total monthly payment stays the same.

This is so that the payments are dispersed equally over the repayment period by these lenders, who amortize The principal you pay down each month increases by the same amount as the interest portion of the bill continues to decline. Consequently, the overall bill stays the same.

Several income-driven repayment options are available from the government; these options are intended to lower payment amounts initially and raise them gradually as your wages rise. In the beginning, you might discover that your loan payments are insufficient to pay off the interest that has accrued over the course of the month. This is what’s known as “negative amortization. ”.

In certain cases, the government will cover all or a portion of the interest that has accumulated but isn’t being paid. On the other hand, the unpaid interest is added to the principal amount annually under the income-contingent repayment plan. Remember that your loan will no longer be capitalized if the amount of your outstanding balance is greater than the initial loan amount.

How to Pay Less Interest on Student Loans

Over the course of the loan, you will pay less interest the more you contribute to the principal balance of your student loans. However, thats not always doable. See if you can refinance your student loans to receive a lower interest rate if you are unable to make additional monthly or annual payments.

It’s not always a good idea to refinance because you might lose some of the protections provided by federal student loans. However, you might be able to get a lower interest rate through refinancing if you have private student loans. Examine the top student loan refinancing companies and determine which option will work best for your budget.

Who Sets Rates for Federal Student Loans?

Federal law, not the U.S. government, determines interest rates on federal student loans. S. Department of Education. They are determined by adding a percentage to the yield on the 10-year Treasury note.

Should I Consolidate My Student Loan for a Better Rate?

It depends. Consolidating your debts can make your life easier, but you must proceed cautiously to protect any benefits you may presently receive from the loans you are carrying. To begin, ascertain whether you qualify for a consolidation. You have to be in school full-time or less than part-time, be in the loan grace period and not in default, and be paying your loans on time.

Can I Deduct Student Loan Interest?

Yes. Depending on their filing status, income level, and interest paid, individuals may be able to deduct up to $2,500 from their annual taxable income.

The Bottom Line

If your student loan has a standard repayment plan with a fixed rate of interest, calculating the amount of interest you owe will be easy. You can always inquire with your loan servicer about how different repayment plans will impact your expenses if you’re interested in reducing the total amount of interest you pay back over the loan’s term. Article Sources: Investopedia mandates that authors cite original sources to bolster their claims. These consist of government data, original reporting, white papers, and conversations with professionals in the field. When appropriate, we also cite original research from other respectable publishers. You can read more about the guidelines we adhere to when creating impartial, truthful content in our

You consent to the use of cookies on your device to improve site navigation, track user activity, and support our marketing initiatives by selecting the option to “Accept All Cookies.”

FAQ

What is the formula for daily APR?

If your monthly APR rate is 17 and your current balance is $500, 99% of the time, you can calculate your daily periodic rate by dividing your current annual percentage rate by 365. In this case, your daily APR would be approximately 0. 0492%. By multiplying $500 by 0. 00049, you’ll find your daily periodic rate is $0. 25.

What is the daily balance method of interest calculator?

One popular method for figuring out credit card interest is the average daily balance method. It is determined by looking at the balance due on the card for each day of the billing cycle. The daily periodic rate on the card and the number of days in the billing period are multiplied by the average daily balance.

What is the formula for calculating interest on a loan?

Interest = Principal × Rate × Tenure is the formula used to calculate interest rates. The interest rate on loans or investments can be found using this formula. What benefits does utilizing a loan interest rate calculator offer?

How do you calculate daily per diem on a loan?

By multiplying the loan balance by the interest rate and dividing the result by 365, you can find the per diem interest. Generally speaking, using an amortization program like TValue software is simpler and more accurate.

Read More :

https://www.investopedia.com/how-to-calculate-student-loan-interest-4772208