We are an independent, advertising-supported comparison service. Our objective is to empower you to make confident financial decisions by giving you access to interactive tools and financial calculators, publishing original and unbiased content, and allowing you to conduct free research and information comparisons.

Issuers that Bankrate has partnerships with include American Express, Bank of America, Capital One, Chase, Citi, and Discover, among others.

What is a VA Construction Loan?

With the help of a VA construction loan, veterans can buy land and use it to construct a unique home that will serve as their primary residence. There are frequently separate closings (and related closing costs) for the permanent mortgage and the VA construction financing.

Before construction starts, it is also possible for the construction loan and permanent financing to be handled with a single loan at closing. We refer to this as a VA construction to permanent loan, or one-time close.

Remember that locating a legitimate VA construction loan might be challenging.

VA Construction Loan Requirements

To be eligible for a VA new construction loan, you must fulfill all of the standard VA loan requirements as well as a few more that aren’t applicable to regular VA loan home purchases.

VA loan new construction requirements include:

- Finding a licensed and insured VA-approved builder

- submitting an application to your lender along with a full set of construction plans

- Appraising the home construction plans

- Providing any additional documentation your lender may require

VA Construction Loan Uses

Veterans who own land or intend to buy it can utilize a VA construction loan to construct a single-family home. Nevertheless, there are limitations on using a VA loan to buy land. Veterans cannot use a VA loan to purchase land unless they plan to start building as soon as they make the purchase.

What is the VA Construction Loan Process?

Every homebuyer’s circumstances are unique and rely on a variety of factors, including the lender they are working with and the home builder.

Generally, the process follows along these lines:

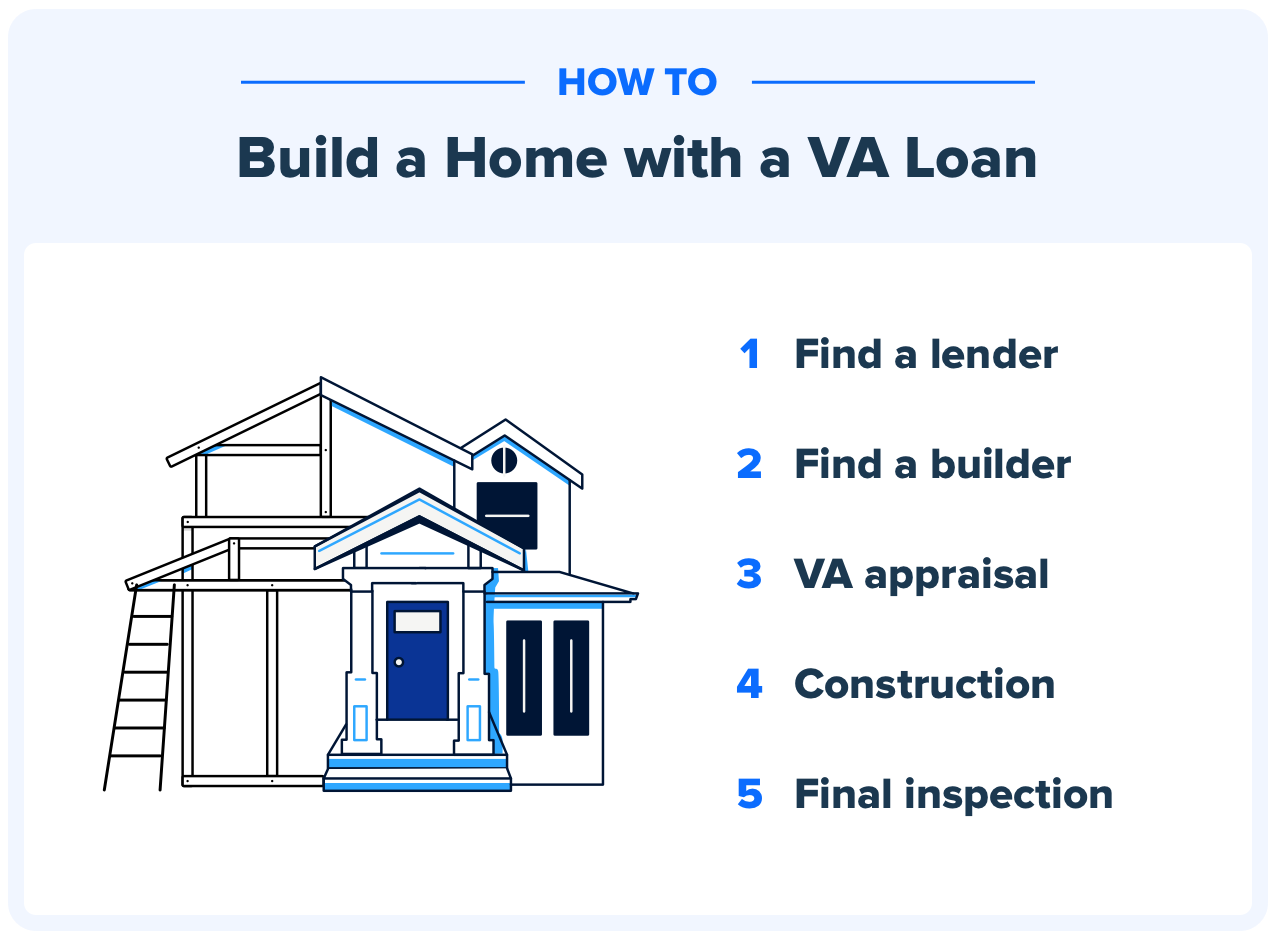

How to Build a Home with a VA Loan

This first step can prove challenging. Many VA lenders do not offer financing for new construction. In the next section, we’ll look at more options for using your VA loan benefit to construct a house.

Lenders may differ in their requirements for credit scores, interest rates, and other factors. You will collaborate with the lender to close the loan before construction begins if you find a reliable source for these loans. This entails submitting the same documentation of employment, income, and finances as you would for a conventional VA purchase loan.

Step 2: Find a Builder

Although home builders are not approved by the VA, they must register with the agency and receive a VA Builder ID. These can usually be obtained within a matter of days. On its website, the VA lists the home builders that have been approved. The construction plans will be given to the lender by you or your builder.

Step 3: VA Appraisal

Based on the new build plans and specifications, the lender will request a VA appraisal. The formal Notice of Value, which states the home’s fair market value, is soon after issued by the VA. Lenders will only lend the amount that is less than the house’s fair market value or its acquisition costs. Your loan can proceed to closing once this crucial step is finished and the proposed home satisfies VA requirements.

Veterans close on a genuine VA construction loan prior to the start of construction. After that, the lender pays a builder to cover the various stages of building a new home.

Step 5: Final Inspection

A final inspection is required by the VA once the home is finished. The original appraiser typically conducts the final inspection whenever possible. With this inspection, you can be sure that the house was constructed in accordance with the right plans and specifications and still satisfies VA’s minimum property requirements.

What if You Can’t Find a VA Construction Loan?

Although the VA insures a portion of each loan, the specific VA lenders choose the types of loans they will offer. Many VA lenders tend to shy away from new construction due to the high level of risk involved.

Veterans United does not offer VA construction loans for the construction of new homes, similar to many other lenders.

Obtaining a construction loan from a builder or a local lender and then refinancing it into a permanent VA loan is an alternative to applying for a VA construction loan.

This approach is something we help Veterans with every month. Here’s what you need to know.

Start with a Construction Loan

If veterans are having trouble finding a lender who will approve a VA construction loan, they can apply for a conventional construction loan and convert it to a VA loan once the deal closes.

Getting a traditional construction loan often requires a down payment. But in some circumstances, it might be able to recover the down payment.

It can be beneficial to compare loans when looking for a construction loan. Speak with several lenders and builders to compare closing costs, down payment requirements, and other details.

Certain builders might provide special offers or programs for veterans and families of service members. Make sure you are working with a reputable builder who has a successful track record and happy homeowners by doing your research.

Any equity that veterans and service members have may be applied toward the down payment requirements for construction financing if they own the land on which they wish to build.

For veterans without land already, buying land can frequently be financed as part of their overall construction loan.

Its important to understand that construction loans are short-term loans. Thus, it is imperative that veterans and active military personnel begin working on the long-term funding as soon as possible.

Permanent VA Financing for Construction Loans

To convert that construction loan from a short-term to a permanent VA loan, lenders have two options. There are two options available: a VA purchase loan or a VA Cash-Out refinance loan. Guidelines and policies on this can vary by lender.

There is not much of a difference between a VA Cash-Out refinance and a VA purchase from an underwriting standpoint. The same underwriting requirements that apply to Veterans buying an existing home also apply to them if they want to convert their construction loan into a permanent VA mortgage. This entails fulfilling criteria related to residual income, debt-to-income ratio, credit score, and other areas.

Additionally, similar to a VA construction loan, the home needs to be constructed by a builder with a valid VA builder ID. These arent hard to get, and its even possible for Veterans to build the home themselves. Builders often need to provide a one-year warranty.

Getting a construction loan is a crucial first step, but after the house is built, you’ll need to convert that short-term loan into a long-term mortgage. Thats not something you want to wait to explore.

New Construction Purchase vs. Cash-Out Refinance

The ability to receive cash back at closing is the primary distinction between VA purchase and VA Cash-Out refinance loans.

Lenders will loan the less of the appraised value of the home and the total amount paid for the construction of the home (plus the land loan, if that amount isn’t covered by the construction loan) for a VA purchase loan.

Qualified buyers may be able to borrow up to 100% of the home’s appraised value through a Cash-Out refinance. This implies that military personnel and veterans might be eligible to receive money from the home’s equity at closing, which could assist in covering the initial cost of a down payment or other out-of-pocket expenses.

Let’s take an example where you obtain a $300,000 construction loan for the purchase of the land and building of the new home, and you put down 10% of that amount. After deducting the $30,000 down payment, you will need to borrow an additional $270,000 to pay back the construction loan.

You might be able to borrow $300,000 if the VA appraisal ultimately shows that the house is worth that much. You would then be able to recoup the difference ($30,000 in this case) between what you owe and the appraised value in cash.

Lenders may have different guidelines regarding loan-to-value ratios and other requirements.

Typically, in order to qualify for a refinance at Veterans United, the borrower must be the legal owner of the land the house is built on. Otherwise, we would treat it as a purchase loan.

While some consumers might seize this cash-back offer, others would rather start with a lower loan balance and continue to build equity. Every buyers situation is different.

Facing Low Inventory, More Veterans Consider Building

As the number of available homes drops to its lowest point in almost 25 years, more veterans and active military personnel are considering new construction. According to recent data from the Mortgage Bankers Association, VA mortgage applications for new construction increased marginally in July compared to June, while conventional applications for new construction decreased.

According to Veterans United Home Loans’ most recent Veteran Homebuyer Report, a quarterly national survey of Veterans, service members, and civilians who intend to buy homes in the next three years, building a new home is one of the top three trade-offs that Veterans and service members are willing to make given the inventory shortage.

The following list shows the main concessions that veterans are prepared to make:

An increasing number of veterans are attempting to completely avoid the inventory problem by building a new home with the benefit of their hard-earned home loan. To be sure, it isn’t always an easy road.

You can definitely use the benefits of your VA loan for new construction. However, the procedure isn’t always clear-cut and easy, and some purchasers might require funds for a down payment to get the transaction started.

Check Your$0 DownEligibility Today!

1. realtor. com is running the sweepstakes and assisting with its administration and promotion. 2. NMLS #1907 (nmlsconsumeraccess. org). Not affiliated with Dept. of Veterans Affairs or any government agency. 3. May be subject to tax withholding. See.

FAQ

Can I build my house with VA loan?

Veterans who own land or intend to buy it can utilize a VA construction loan to construct a single-family home. Nevertheless, there are limitations on using a VA loan to buy land. Veterans cannot use a VA loan to purchase land unless they plan to start building as soon as they make the purchase.

What is the minimum credit score for a VA construction loan?

VA Nationwide Home Loans. According to the statement, it provides financing for these loans at 0% interest with a minimum credit score of 20620 and funds the construction phase.

Do VA construction loans require a down payment?

First off, compared to conventional loans, VA construction loans have lower interest rates. Additionally, there is no down payment needed, and those who decide not to put down payment will not be charged for private mortgage insurance (PMI).

Can you use a VA loan to build a Barndominium?

In general, a VA loan can be used to either build or purchase an existing barndominium. The VA’s minimum property and occupancy requirements, in addition to other requirements, must be met by the barndominium. The property being purchased must be used as the primary residence in order to qualify for a VA loan.

Read More :

https://www.veteransunited.com/valoans/va-construction-loans/

https://www.rocketmortgage.com/learn/va-construction-loan