Is student loan interest deductible?

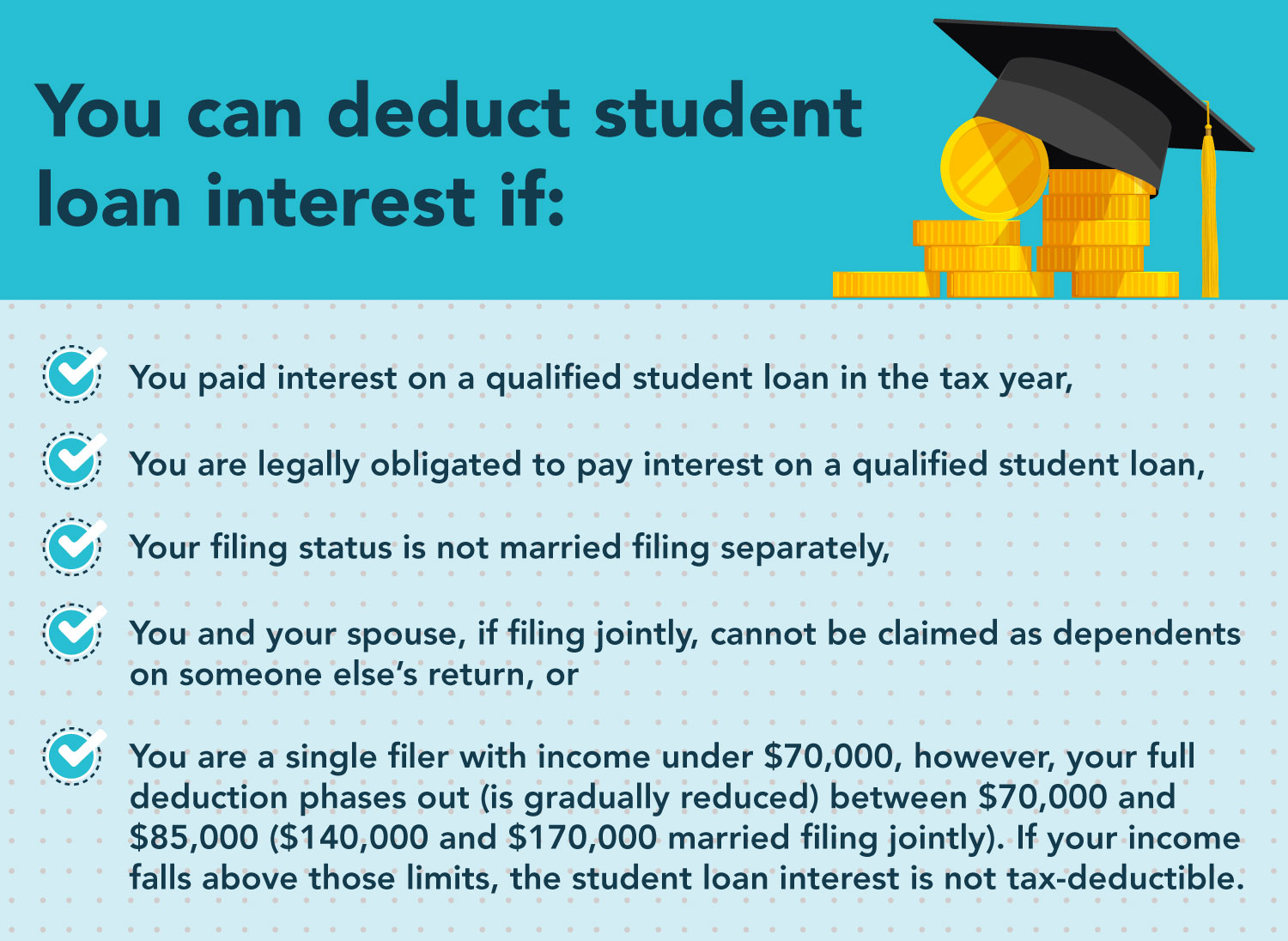

If your modified adjusted gross income, or MAGI, is less than $70,000 ($145,000 if filing jointly), the interest on your student loans is deductible. The maximum $2,500 can be deducted if your MAGI was between $70,000 and $85,000 ($175,000 if filing jointly).

The interest on student loans is deducted above the line and is not itemized. In order to save you money, it is deducted from your taxable income. For instance, should you find yourself in the 2022–2023 tax bracket, the maximum deduction for student loan interest would return $550 to your pocket.

Who can deduct student loan interest?

The following situations allow you to deduct student loan interest paid on federal and private student loans if your MAGI is less than $85,000 ($175,000 if filing jointly):

- You used the loan for qualified education expenses. These consist of books, room and board, tuition, and other required costs like transportation.

- Youre making interest payments while still in school. This deduction isn’t limited to recent graduates filing taxes; you might also be eligible to claim it if you’re an overachiever who is still paying off student loans.

- You took out the loan for a dependent. You are eligible to deduct the interest on your student loans if you took out a loan in your name for someone else, such as a parent PLUS loan for your child.

- You were obligated to repay the loan. You may still deduct any interest you have paid off from your loan balance even if your wages are being garnished or you are otherwise legally obligated to repay the debt.

If you file as a married individual filing separately, you are not eligible to deduct the interest from your student loans. Additionally, if you are claimed as a dependent on another person’s tax return, you are not eligible. Even if the student is listed as a dependent, a parent who is not legally required to pay interest on the loan cannot claim the interest deduction.

The amount of years you can deduct interest from student loans is not limited. If you meet the additional eligibility requirements for the deduction, repay a qualified student loan, and your income is within the limits, you are eligible to take this deduction each year.

Student loan interest deduction form

Form 1098-E, a student loan interest deduction form, will be sent to you automatically by mail or email if you paid more than $600 in interest in 2022.

With federal interest rates at 200 percent and payments suspended for the entirety of 2020, you might have paid less than that amount. But if you otherwise qualify, you can still deduct the amount that you did pay.

Ask your student loan servicer or private lender to send you the interest deduction document if you haven’t received it. You may be able to access a copy of the form through your online account portal, along with information about the amount of interest you paid.

Are student loan payments deductible?

Repaying student loans includes paying off both the initial balance and any accumulated interest. The whole amount of your student loan payments is not tax deductible, but you can write off the interest on your taxes.

Let’s take an example where you have a $29,000 student loan with a 5% interest rate. Upon commencing the standard 10-year repayment plan, your monthly payment would be approximately $308, with approximately $121 going toward interest on your student loans.

You would repay $3,691 in total during the first year of repayment, consisting of $1,398 in interest and $2,293 in principal. You could lower your taxable income by the amount of interest paid on your student loans if you were eligible for the interest deduction.

This covers interest that was capitalized, or added to your balance, when you entered repayment as well as any newly accrued interest, such as that $1,398.

Additional education tax breaks

The government provides additional education tax credits and deductions if you are still enrolled in school or are paying for educational expenses. If you are not eligible for a credit, you may choose to deduct tuition and fees instead of claiming the lifetime learning credit or the American opportunity credit.

You are eligible for these benefits even if student loans were used to cover some of your costs. Which will save you the most can be determined with the help of your income and other variables. Similar to the student loan interest deduction, in order to qualify for these tax benefits if you’re married, you must file your taxes jointly.

Should you refinance your student loans?

You can lower your monthly payment and the amount of interest you pay by refinancing your student loans. Use the calculator below to determine your potential savings if you have private loans. Refinancing federal student loans during the pause in interest and payments is not advised.

![]()

FAQ

Can you write off loan payments on taxes?

While some forms of loans are tax deductible, personal loans are not You can usually deduct interest paid on business, student, and mortgage loans from your annual taxes, which lowers your taxable income for the year.

What student expenses are tax-deductible?

Qualified education expenses Tuition and fees. Room and board. Books, supplies and equipment. Other necessary expenses (such as transportation).

Is student loan interest deductible in 2023?

Your eligibility for an interest deduction on student loans is dependent on your income, and the maximum amount you can claim is $2,500 for 2023 and 2024. That is the maximum amount of interest you can claim, even if you paid more than that during the year.

Is student loan interest deductible on top of standard deduction?

Interest on student loans is deductible as a “adjustment to income.” This implies that it is deducted from your taxable income prior to the claim of the majority of other deductions. Additionally, it implies that you can write off interest from student loans even if you claim the standard deduction on your tax return.

Read More :

https://studentaid.gov/resources/tax-benefits

https://www.consumerfinance.gov/ask-cfpb/do-student-loans-affect-my-taxes-en-623/